文章来源:Xeneta

作者:Peter Sand(Xeneta首席分析师)

Emily Stausbøll(Xeneta高级航运分析师)

翻译:XCLshipping

排版:XCLshipping

Xeneta是一家国际知名的海运和空运运费基准和市场情报服务提供商。Xeneta跟踪北美、欧洲和远东亚洲的长期和即期汇率市场的进出口情况。依靠众包数据,Xeneta的数据库中包含承运商向大量实际客户报价的合同价格和现货市场价格。

Xeneta 是一家新时代的海运和空运运价基准和市场情报服务提供商。Xeneta 跟踪北美、欧洲和远东亚洲的长期和即期汇率市场的进出口情况。

依靠众包数据,Xeneta 的数据库中包含运营商向大量实际客户报价的合同价格和现货市场价格。

Xeneta 是一家新时代的海运和空运运价基准和市场情报服务提供商。Xeneta 跟踪北美、欧洲和远东亚洲的长期和即期汇率市场的进出口情况。

】】】】】Xeneta 是一家新时代的海运和空运运价基准和市场情报服务提供商。Xeneta 跟踪北美、欧洲和远东亚洲的长期和即期汇率市场的进出口情况。依靠众包数据,Xeneta 的数据库中包含运营商向大量实际客户报价的合同价格和现货市场价格。

近日,Xeneta发布一份《2025年航运展望》(2025 Ocean Outlook Report),在海运集装箱航运市场经历了艰难的一年之后,2025年,航运业将迎来风平浪静的水域,还是面临进一步的中断和挑战?Xeneta这份行业展望提供了其关于影响未来一年市场关键因素的重要见解。

报告预计,2024年的集装箱总需求增长率将达到4%~5%,突破1.8亿个标准箱,超过2021年1.798亿个标准箱,达历史最高水平。Xeneta分析师认为,这主要是因为托运人大量提前装载货物出口,确保有足够的货物库存,以保障供应链。

展望 2025 年,毫无疑问,这可能是海运集装箱运输又一个充满挑战的一年。

When looking ahead to 2025, there can be no sugar-coating the likelihood of it being another challenging year in ocean container shipping.

如果 2024 年是红海冲突的一年,那么预计还会有更多类似的情况,因为没有迹象表明有政治解决方案允许集装箱船大规模返回该地区。

这只会增加集装箱运输的危险,因为系统几乎没有余力来应对另一次供应链冲击。

《Xeneta 2025 年海洋展望》明确了绕道非洲对运力需求和市场可用运力的影响。新船舶的交付和标准箱数量增长的放缓将在一定程度上减轻这一负担,但不足以缓解另一场重大事件。

我们会看到台海军事升级吗?孟加拉国政权更迭是否会引发进一步动荡?中东局势恶化是否会影响波斯湾航运?地缘政治仪表板上的红灯闪烁,忽视它们是愚蠢的。

必须将其他因素添加到其中。

美国对中国商品征收新关税的可能性或许会导致运费飙升,托运人会争相提前进口。我们是否会看到中国对墨西哥的需求持续增长成为进入美国的“后门”?一月份美国东海岸和墨西哥湾沿岸港口进一步罢工的威胁也越来越大。

另一个值得关注的问题是托运人、货运代理和承运人对 2025 年第一季度推出的新联盟有何反应。

自 7 月份达到顶峰以来,远东地区主要航线的现货市场一直在走软,这对于即将进行的新长期合同谈判的托运人来说是个好消息。然而,不需要太多的时间就能将指针推回到红色警戒区,并使航运市场运价再次螺旋式上升。

对托运人有利的一个因素是他们可以获得比以往更多的数据和洞察力。这意味着他们可以根据时间表可靠性、运力、运输时间和二氧化碳排放来密切监控各个航线和主要承运商的货运支出。

2024 年对托运人来说是痛苦的一年,他们希望 2025 年能有所缓解,但重要的是要面对现实并为进一步的混乱做好准备。

《Xeneta 2025 年海洋展望》将强调面对海运集装箱运输市场的不确定性时需要考虑的关键因素和风险,以便您可以保持供应链运转、有效管理预算并维持良好的供应商关系。

If 2024 has been a year framed by conflict in the Red Sea, then expect more of the same because there is no sign of a political resolution that would allow a large-scale return of container ships to the region.

This only heightens the danger for container shipping because there is little slack in the system to deal with another supply chain shock.

The Xeneta Ocean Outlook 2025 makes clear the impact diversions around Africa have on TEU-mile demand and available capacity in the market. New deliveries of ships and slowing TEU-volume growth will ease some of this burden, but not enough to mitigate another major incident.

Could we see a military escalation in the Taiwan Strait? Will regime change in Bangladesh cause further unrest? Will the situation in the Middle East deteriorate to impact shipping in the Persian Gulf? The lights are flashing red on the geo-political dashboard and it would be a foolish to ignore them.

Other factors must be added into the mix.

The potential for new US tariffs on Chinese goods could see a spike in freight rates and shippers rushing to frontload imports. Will we see continued demand growth from China to Mexico as a ‘back door’ into the US? The threat of further strike action at ports on the US East Coast and Gulf Coast in January also looms large.

Another one to watch is how shippers, freight forwarders and carriers react to the new alliances as they are rolled out in Q1 2025.

Spot markets have been softening on major fronthauls out of the Far East since peaking in July, which is good news for shippers ahead of new long-term contract negotiations. However, it will not take much to push the needle back into the red alert zone and the logistic markets to spiral once again.

One factor working in shippers’ favor is that they have access to more data and insight than ever before. This means they can closely monitor freight spend on individual corridors and benchmark carriers against schedule reliability, capacity, transit times and CO2 emissions.

2024 has been a bruising year for shippers and they will hope 2025 brings some relief - but it is important to be realistic and prepare for further disruption.

The Xeneta Ocean Outlook 2025 will highlight the key themes and risks to consider in the face of ocean container shipping market uncertainty so you can keep supply chains moving, manage budgets effectively and maintain good supplier relationships.

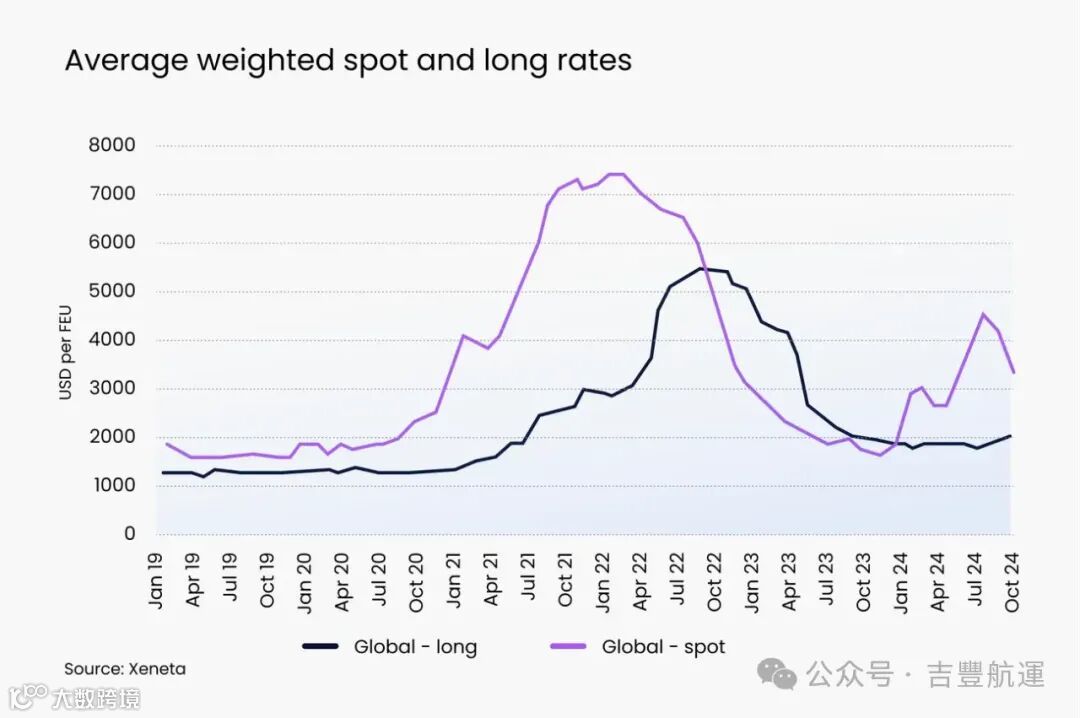

随着航运期货市场开始上涨,根据Xeneta 平台数据显示全球现货市场运费自 7 月份达到峰值以来已经走弱。

在2025年新的长期合同谈判之前,多空市场的收窄将具有重要意义。

托运人将希望市场进一步收窄,而承运人则竭尽全力保持现货市场的高位运行。

Xeneta's global average spot rate has softened since peaking in July as the long term market begins to rise.

The narrowing of the long-short market will be of great significance ahead of negotiations for new long term contracts in 2025.

Shippers will be hoping the markets narrow further while carriers are doing their utmost to keep the spot market elevated.

Source: www.xeneta.com

宏观展望:全球集装箱量增长在创纪录的 2024 年后将略有放缓

Macro outlook: Growth in global container volumes to slow slightly after record-breaking 2024

2025年需求将增长3%

Demand to grow by 3% in 2025

宏观经济发展为集装箱运输需求确定了总体方向,但托运人需要了解市场的细微差别。

Macro-economic developments set the overall direction for container shipping demand but shippers need to understand market nuances.

红海冲突对标箱量-英里需求的影响

Impact of Red Sea conflict on TEU-mile demand

部分返回红海将使标箱量-英里需求变化在 +3% 至 -11% 之间

Partial return to Red Sea would see TEU-mile demand change of between +3% and -11%.

船舶大规模返回红海目前看来是不可想象的,但在 2025 年的某个时候部分返回是可能的。

A large-scale return to the Red Sea seems inconceivable at present, but a partial return may be possible at some point in 2025.

运力:创纪录的船队增长将在2025年放缓

Capacity: Record fleet growth to slow in 2025

2025年运力增长将放缓至 4.5%

Fleet growth to slow to 4.5% in 2025

到 2025 年,航运公司对船队采取了截然不同的方法,因此不可避免地会出现一些赢家和一些输家,具体取决于市场的发展方式。

Carriers have taken very different approaches to fleet in 2025, so there will inevitably be some winners and some losers depending how the market develops.

航运联盟:选择合适的服务提供商变得更加复杂

Alliances: Choosing the right service provider just got more complicated

2025年联盟的重大变化

Major changes to Alliances in 2025

保持选择余地,不要害怕挑战运营商,并寻求他们能够兑现承诺的保证。

Keep your options open, do not be afraid to challenge carriers and seek assurances they can deliver what they are promising.

中断:需要管理的风险清单越来越长

Disruption: List of risks to manage keeps getting longer

红海将继续影响供应链

Red Sea will continue to impact supply chains

聪明的托运人已经从疫情中吸取了教训,并正在采取新的数据驱动方法来进行货运采购和供应链风险管理。

Smart shippers have learned lessons from the pandemic and are taking a new data-driven approach to freight procurement and supply chain risk management.

脱碳与环境监管

Decarbonization & environmental regulation

欧盟碳排放交易体系将在2025年扩大覆盖70%的二氧化碳

EU ETS ramps up in 2025 to cover 70% of CO2

托运人必须了解其服务提供商的碳排放策略,并且不要害怕质疑添加到其全包运费中的任何附加费。

Shippers must understand the carbon emissions strategy of their service provider and not be afraid to question any surcharge that is added to their all-in freight rate.

1. 宏观展望:全球集装箱量增长在创纪录的 2024 年后将略有放缓

1. Macro outlook: Growth in global container volumes to slow slightly after record-breaking 2024

-

-

2024年总需求增长将达到 4-5% 并突破 180百万标准集装箱

-

-

整体通胀率将保持在欧洲央行和美联储设定的 2.0% 阈值以上

Demand to grow by 3% in 2025

Total demand growth for 2024 to land at 4-5% and break though 180m TEU

Massive demand growth from China to Mexico expected to continue

Overall inflation to stay above 2.0% threshold targeted by the European Central Bank and Federal Reserve

2024年前八个月的全球集装箱需求同比增长6.7%,其中5月和8月均超过了16百万标准箱大关,这在以前从未发生过。(来源:CTS)

Xeneta预计2024年的总需求增长将达到4-5%,并突破180百万标准箱,超过2021 年以来 179.8 百万标准箱的历史新高。

2024年是托运人大量提前装载货物的一年,以保护供应链并确保在更严重的中断即将到来时有足够的货物库存。

Global demand in the first eight months of 2024 was up 6.7% year-on-year, with May and August both surpassing the 16m TEU mark, which had never happened before. (source: CTS)

Xeneta expects total demand growth for 2024 to land at 4-5% and break through 180m TEU, surpassing the all-time high of 179.8m TEU from 2021.

2024 has been a year characterized by shippers’ extensive frontloading of cargo to safeguard supply chains and ensure enough goods were on inventory should even worse disruptions be on the way.

贸易与GDP的乘数为1.6,是自2011年以来的最高水平,明显突破了 2012-2023年的平均水平0.8。这强化了这样一种观点,即提前进口是为了保护供应链,而不是由于潜在的消费者需求。这表明,随着托运人减少库存,2025年的进口量将减少。

Xeneta预测,到2025 年,全球标准箱需求将增长3%。

A trade-to-GDP multiplier at 1.6 is the highest since 2011, representing a clear trend-break from the 2012-2023 average of 0.8. This reinforces the suggestion that frontloading of imports was to protect supply chains rather than due to underlying consumer demand. This would suggest lower imports in 2025 as shippers draw down on inventories.

For 2025, Xeneta forecasts a 3% TEU demand growth on a global level.

到2025年,美国的后门将保持开放

Back door to the US will remain open in 2025

2024年,中国与墨西哥的贸易备受关注,与2023年相比,年初至今的 标箱量-英里需求增长了22.1%。这是继2023年全年同比增长34.6%之后的又一增长。

其中一个关键原因是中美关系降温,墨西哥被视为规避进口关税的后门。展望2025年,预计该贸易的需求将进一步增加。

另一个值得关注的是中国到中东的货运量,其货运量比2021年增长了 52%。

China to Mexico trade has been in the spotlight in 2024 with TEU-demand growth increasing 22.1% year-to-date compared with 2023. This follows full year-on-year growth of 34.6% in 2023.

One of the key reasons is found in the cooling relations between China and US and Mexico being seen as a backdoor to avoid import tariffs. Looking ahead to 2025, demand is expected to increase further on this trade.

Another one to watch is China to the Middle East where volumes are 52% up from 2021.

• Euro Area GDP growth set to climb to 1.5% in 2025 from low base of 0.9%, while it is sliding downwards in the US to 1.9% from an expected level of 2.6% in 2024.

• Overall inflation has come down from the peaks of 2022/2023, and more importantly it is now mostly on services rather than goods.

• Overall inflation looks like it will stay above the 2.0% threshold targeted by the European Central Bank and Federal Reserve, so consumers may still struggle to go on buying sprees.

• Wage growth in 2025 is expected at 3.4% for the Euro Area (4.3% in 2024) and 2.5% in the US (2024: 3.2%).

• Don’t pay too much attention to the overall Chinese economy – there is more insight to be gained assessing the economic outlook of nations its containerized goods are being exported to.

2025 年可能增加需求的因素:

可能对 2025 年需求产生不利影响的因素:

Factors which could increase demand in 2025:

Faster decline in US inflation

Recovering German economy

Disruption such as natural disaster and geopolitical events

Factors which could adversely impact demand in 2025:

Retailers normalizing inventories after 2024 frontloading of cargoes

Geopolitical deterioration / imposing of new sanctions

Consumers being fearful of the future. including rising unemployment in the US

Interest rates not cut fast enough in US and Euro Area

“宏观经济发展为集装箱航运需求设定了总体方向,但它并不能说明全部情况,托运人需要了解区域和港口到港口层面的市场细微差别。即将到来的美国总统大选将对 2025 年产生重大影响,因为对中国进口商品征收新关税的可能性或许会使托运人重新审视其制造和供应链设置,并可能看到对墨西哥的进口进一步加速。

“2024年,除了更长的航行距离外,还受到货物预装的推动。明年这种方法的任何变化都代表着需求下降的风险——除非2025年变得更加剧烈。”

“Macro-economic developments set the overall direction for container shipping demand but it does not tell the whole story and shippers need to understand market nuances at a regional and port-to-port level. The upcoming US Presidential elections will have a major influence on 2025 because the potential for new tariffs on Chinese imports could see shippers revisit their manufacturing and supply chain set ups – and perhaps see a further acceleration in imports to Mexico.

“2024 was very much driven by frontloading of cargoes, in addition to longer sailing distances. Any change in this approach next year represents a downward risk to demand – unless 2025 turns out to be even more dramatic.”

2. Impact of Red Sea conflict on TEU-mile demand

-

如果船舶返回红海,运力将持续面临压力,但新船交付会缓解压力

-

到 2025 年,大规模返回红海将使标箱量-英里需求减少 11%

-

部分返回红海时,标箱量-英里需求将变化 +3% 至 -11% 之间

-

-

如果一些中国承运商返回红海,而欧洲承运商继续往非洲绕航,市场将看到有趣的动态

-

No return of ships to Red Sea would see continued pressure on capacity, but eased by new deliveries

-

Large-scale return to Red Sea would see TEU-mile demand reduce by 11% in 2025

-

Partial return to Red Sea would see TEU-mile change of between +3% and -11%

-

Large scale return is least likely scenario

-

Market would see intriguing dynamic if some Chinese carriers return while European carriers continue to divert around Africa

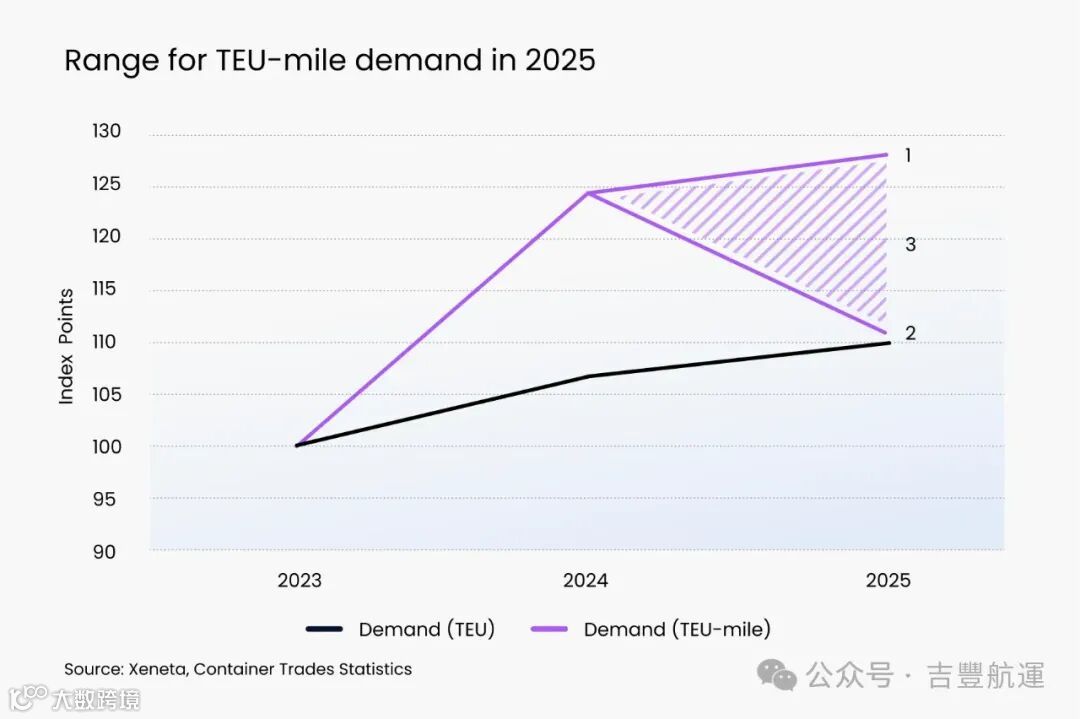

红海的情况意味着,仅仅关注移动的集装箱数量并不能揭示集装箱运输的全貌。

相反,我们必须考虑标箱量-英里需求,该需求考虑了每个标准集装箱的运输距离和运输数量。

随着船舶绕道非洲好望角,2024年标箱量-英里需求激增,这也使得许多原本可能导致市场产能过剩的船舶有了工作可做。

到2025年,标箱量-英里需求将继续成为了解运费变化背后的动态的关键因素。

The situation in the Red Sea means purely focusing on the number of containers moved does not reveal the full picture for container shipping.

Instead, we must consider TEU-mile demand, which factors the distance each container is transported as well as the number transported.

TEU-mile demand shot up in 2024 as ships diverted around the Cape of Good Hope and was the reason many ships that would otherwise have contributed to overcapacity in the market in 2024 had work to do.

In 2025, TEU-mile demand will continue to be a key factor in understanding the dynamics behind shifting freight rates.

在我们的 2025 年展望中,我们探讨了三种可能的情况:

-

-

-

For our 2025 Outlook, we explore three potential scenarios:

No return of container ships to the Red Sea

Full return of container ships to the Red Sea

Partial return of container ships to the Red Sea

出现此情景的原因

-

以胡塞武装袭击红海船只为背景的更广泛的中东冲突正在升级,且未见解决的迹象。

-

自红海危机开始以来已造成多人死亡,承运商将关注袭击对其船员和船舶构成的风险。

对运输的影响

-

平均航行距离将与2024年大致相同,这意味着标箱量-英里需求的增长将紧随以货运量衡量的增长。

-

-

-

Scenario 1: No return of container ships to the Red Sea

Freight rates continue to ease as growing fleet absorbs diversions.

Reasons for this scenario to play out

-

Conflict in the wider Middle East, which formed the backdrop for Houthi attacks of ships in the Red Sea, is escalating and showing no signs of a resolution.

-

Carriers will be mindful of the risk attacks pose to their crew and ships, with multiple fatalities since the crisis began.

-

Average distance sailed will remain broadly the same as in 2024, which means growth in TEU-mile demand will closely follow growth measured in volumes.

-

Capacity tightness will ease as new ships are delivered.

-

Longer transit times now built into supply chains.

-

Freight rates continue to ease as growing fleet absorbs diversions.

如果认为威胁已经过去,主要航线的船舶会在短时间内返回红海。

出现此情景的原因

在宣布2025年的服务时,几家航运公司发布了两个版本——一个是船只继续绕道好望角航行,另一个是穿越红海。尽管如此,几乎没有其他迹象表明2025年可能会完全返回红海。

对运输的影响

-

平均航行距离下降到危机前的水平,导致 标箱量-英里需求下降。即使全球货运量增长 3%,标箱量-英里需求也将比2024年下降 11%。

-

-

-

以前因绕道占用的运力将被释放出来,导致市场供过于求。

-

除非承运商们能有效地管理运力,否则运费会下降,但这并非易事。

-

Scenario 2: Full Return

Major carriers return to the Red Sea in a short period of time if threat is deemed to have passed.

Reasons for this scenario to play out

In announcing their 2025 services, several carriers published two versions - one where ships continue to sail around the Cape of Good Hope and the other going through the Red Sea. Despite this, there is little else to suggest a full return is likely in 2025.

-

Average sailing distance drops to pre-crisis levels which leads to a drop in TEU-mile demand. Even with 3% growth in global volumes, TEU-mile demand would be down 11% from 2024.

-

Congestion at major ports in the immediate period following a return to Red Sea.

-

Shippers adjust to a return of shorter transit times.

-

Capacity previously absorbed by the diversions is freed up which floods the market.

-

Freight rates drop unless carriers are very effective at managing capacity, but this would be difficult.

-

Charter rates drop and demolition increases.

如果某些承运商认为风险足够低,他们会选择重返红海。一家承运商重返红海并不意味着其他承运商也会效仿,如果他们评估自己船队风险更高的话。

出现此情景的原因

与中国有关联的船舶风险等级较低。因此,即使中国承运商中远集团在2025年全面重返红海,欧洲承运商也不一定会效仿。

对运输的影响

-

假设2025年全球货运量增长3%,这将导致标箱量-英里需求同比变化+3%至-11%。

-

运力压力缓解,对租船市场和拆船活动产生更广泛的影响。

-

-

随着各航运公司对其船队进行单独调度,新的联盟关系也随之调整。

Scenario 3: Partial return

Select carriers choose to return if they deem the risk low enough. One carrier returning to the Red Sea does not mean other carriers will follow if they deem their risk profile to be higher.

Reasons for this scenario to play out

China-affiliated ships are at the lower end of the risk scale. Therefore, even if the Chinese carrier COSCO makes a full return in 2025, European carriers will not necessarily follow.

-

Assuming global volume growth of 3% in 2025 this would lead to a year-on-year change in TEU-mile demand of between +3% and -11%.

-

Easing of pressure on capacity, with wider impact on charter market and demolition activity.

-

Freight rates to ease unless carriers can successfully manage capacity.

-

New alliances adapt as individual carriers make individual calls on their fleet.

艾米丽·斯托斯博尔 Emily Stausbøll

Senior Shipping Analyst, Xeneta

“目前似乎无法想象船舶大规模返回红海,但在2025年的某个时候可能会部分返回。这将引发一个有趣的市场动态,托运人将面临选择,要么通过苏伊士运河使用运输时间更短的承运人,要么坚持选择继续在好望角绕道的承运人。有很多事情需要考虑,尤其是对于那些可能开始失去市场份额的承运商来说,这些竞争对手已经重返红海。”

“A large-scale return to the Red Sea seems inconceivable at present, but a partial return may be possible at some point in 2025. This will throw up an intriguing market dynamic with shippers facing the choice of utilizing trades with shorter transit times via the Suez Canal or sticking with carriers who continue to divert around the Cape of Good Hope. There will much to consider, not least for the carriers who may begin to lose market share to competitors who have returned to the Red Sea.”

3. Capacity: Record fleet growth to slow in 2025

船队增长将在2025年放缓至4.5%,不到2024年增长的一半

到2025年底,全球海运集装箱船队的吞吐量将达到3270万标准箱

MSC将巩固其全球最大运力的航运公司地位

OCEAN Alliance 将在2025年交付大部分运力

200,000 TEU 将计划拆船

只要继续前往非洲绕航,运力将保持紧张,但新交付的运力将缓解这状况

航运公司可能很难找到船只来扩充他们的船队

-

Fleet growth to slow to 4.5% in 2025, less than half the growth in 2024

-

Global ocean container shipping fleet to hit 32.7 million TEU by the end of 2025

-

MSC to strengthen status as world’s largest carrier

-

OCEAN Alliance to have most capacity delivered in 2025

-

200 000 TEU to be removed through demolition

-

As long as diversions around Africa continue, capacity will remain tight but will be eased by new deliveries

-

Carriers may struggle to find ships to add to their fleet

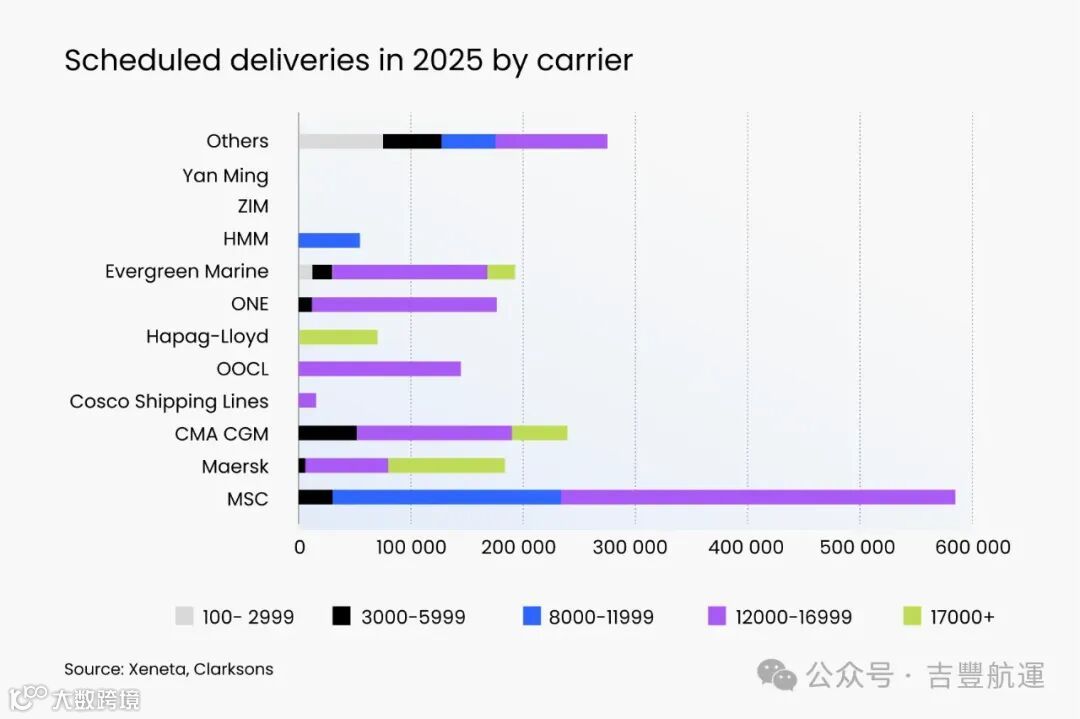

MSC是预计新增运力最多的单一承运商,计划在2025*年以46艘新船的形式交付582,000标准箱(来源:Clarksons)。绝大多数新增船舶由MSC拥有,其中 9 艘船由非经营性船东(NOOs) 拥有并租给MSC。这些交付运力将扩大MSC作为全球最大航运公司的地位,新增运力将提升其目前20%的市场份额,使其从2025年起能够尝试采取非联盟策略。

OCEAN 联盟 - 唯一不变的联盟,在2025年将交付最多的运力。组成该联盟的三家承运商(中远集团、达飞海运和长荣海运)计划明年交付 591,000 标准箱。

新的"Premier"联盟 - 在失去赫伯罗特后已经是最小的联盟,新船将交付的运力最低,“仅”230,000 TEU。从该联盟中三家承运商的详细信息来看,ONE占176,000TEU,其余为 HMM,这意味着阳明航运在 2025 年没有交付计划。事实上,阳明航运的订单本上只有5艘船,这5艘15500 TEU LNG双燃料集装箱船新船都将在 2026 年交付。

唯一一家不期待任何新船的前 10 名运营商是以星航运。它正在等待 2024 年交付六艘船,其中一些可能要到 2025 年才能交付,但没有之后的新船订单。

The carriers and alliances driving fleet growth

MSC is the single carrier expecting the most new tonnage, with 582 000 TEU scheduled for delivery in 2025* in the form of 46 new ships (source: Clarksons). The vast majority are owned by MSC with nine owned by non-operating owners (NOOs) and chartered to MSC. These deliveries will extend MSC’s status as the globe’s largest carrier, with the new deliveries adding to its current market share of 20% affording it the scale to attempt a non-alliance approach from 2025.

OCEAN Alliance - the only unchanged alliance - will see the most capacity delivered in 2025. The three carriers that make up the alliance (COSCO Group, CMA CGM and Evergreen) have 591 000 TEU scheduled for delivery next year.

The new Premier Alliance - already the smallest alliance after losing Hapag-Lloyd - will see the lowest deliveries of new ships at ‘only’ 230 000 TEU. Looking into the details of the three carriers in this alliance, ONE accounts for 176 000 TEU with HMM making up the remainder, meaning Yang Ming has no deliveries scheduled in 2025. In fact, Yang Ming only has five ships in its orderbook, all 15 500 LNG capable ships to be delivered in 2026.

The only other top 10 carrier not expecting any ships is ZIM. It is waiting for the delivery of six ships in 2024, some of which may only arrive in 2025, but after that has an empty orderbook.

租船市场

在运力前10航运公司中,以星航运的包租运力比例最高,为 91.3%,阳明航运以 56.9% 位居第三(来源:Alphaliner)。其他航运公司也严重依赖租船市场,但这通常是在订购船舶时与非经营性船东(NODs)达成长期协议。

以星航运和阳明航运在2025年扩大船队的任何雄心都将依赖于短期租船市场——但这种选择是有限的。Alphaliner 报告称,截至9月底,全球船队中只有0.6%处于闲置状态,其中只有一艘是3000TEU 以上的非经营性船东拥有的船舶。

目前,一艘 6800TEU船舶的平均租赁费率为每天67500美元,合同期限为6-12个月。

依赖租船市场对承运人有好处,但当市场紧张时,他们可能很难在最想扩充船队的时候找到可用的运力。

Charter market

Out of the top 10 carriers, ZIM has the highest share of chartered capacity at 91.3% with Yang Ming in third place at 56.9% (Source: Alphaliner). Other carriers also rely heavily on the charter market, but this is often on long-term arrangements agreed with NOOs at the time of the ship being ordered.

Any ambitions ZIM and Yang Ming may have to grow their fleets in 2025 will rely on the shorter term charter market – but this option is limited. Alphaliner reports that, as of the end of September, only 0.6% of the global fleet is idle, of which only one is an NOO ship above 3 000 TEU.

The average charter rate for a 6 800 TEU ship is currently USD 67 500 per day for a 6-12 month contract.

A reliance on the charter market has benefits to carriers, but when the market is tight, they can struggle to find available tonnage at a time when they are most keen to add to their fleet.

拆船市场

2024年前9个月,被拆除船舶的平均年龄为29.2岁。这高于2020年至2023年的26.5年,远高于之前四年的平均21.8年。

了解拆船市场前景的关键在于租船费率。在过去五年的大部分时间里,对吨位的高需求意味着租船费率一直很高,从而延长了老旧和效率较低的船舶的使用寿命,因为当租船费率较高时,这些老船也会盈利。

有些人会争辩说,一旦运力紧张状况缓解,承运人将转向拆船来重新平衡船队,以适应运输需求。然而,即使我们假设恢复到疫情前的平均水平,并假设目前超过22年船龄的船舶中有四分之三将被送往拆解,这将导致180万TEU运力退出市场。

即使如此高水平的拆除也不足以扭转承运商的命运,因为如果返回红海,而且鉴于过去四年交付了数百万标准箱,市场不可避免地会出现运力过剩。

即使在如此高比例的拆船情况下,也不足以扭转承运商的命运。如果重返红海,而鉴于过去四年交付的数百万TEU运力,市场将不可避免地会出现运力过剩。

注释:*预期交付包括 Xeneta 估计的 10% 的合同将被取消,10% 的合同将推迟到下一年,而计划交付包括所有交付日期在 2025 年的船舶。

Demolition

In the first nine months of 2024, the average age of ships being demolished is 29.2. This is up from the 26.5 between 2020 and 2023, which was much higher than the previous four-year average of 21.8 years.

The key to understanding the outlook for demolition is found in charter rates. High demand for tonnage during much of the past five years mean charter rates have been high, extending the lifetime of older and less efficient ships as even they will be profitable when charter rates are high.

Some will argue that once the strain on capacity eases, carriers will turn to demolition to re-balance the fleet to match that of demand for transportation. However, even if we assume a return to the pre-pandemic average, and assume three-quarters of ships currently over 22 years will be sent for demolition, this would result in 1.8m TEU leaving the fleet.

Even this high level of demolition would not be enough to turn carrier fortunes around in the case of a return to the Red Sea and the inevitable overcapacity in the market given the many millions of TEU delivered over the past four years.

Footnote: *Expected deliveries include Xeneta’s estimates that 10% of contracts will be cancelled and 10% delayed to the following year, whereas scheduled deliveries include all ships with a delivery date in 2025.

艾米丽·斯托斯博尔 Emily Stausbøll

Senior Shipping Analyst, Xeneta

“2025 年,承运商对船队采取了非常不同的方法,因此不可避免地会有一些赢家和一些输家,这取决于市场的发展情况。这种情况为托运人创造了机会,只要他们了解如何利用不同的承运商和联盟策略来发挥自己的优势。虽然市场仍然紧张,但拥有最大运力的承运人将占据优势,但运力紧张有所缓解——尤其是大量船舶返回红海——都将极大地改变这种情况,并给承运商带来压力,迫使他们通过激进的定价来保持市场份额。”

“Carriers have taken very different approaches to fleet in 2025, so there will inevitably be some winners and some losers depending how the market develops. This situation creates an opportunity for shippers as long as they understand how to use the varying carrier and alliance strategies to their advantage. While the market remains tight, carriers with the largest tonnage will have the upper hand, but any easing in capacity – especially through a large-scale return of ships to the Red Sea - would transform the situation dramatically and put pressure back onto carriers to maintain market share through aggressive pricing.”

4. Alliances: Choosing the right service provider just got more complicated

-

-

-

OCEAN Alliance在2025年拥有最多的运力和服务航线

-

-

-

-

Major changes in Alliances in 2025 will bring risk and opportunity

-

Best carrier network will vary tremendously from trade to trade

-

OCEAN Alliance has most capacity and service loops in 2025

-

Gemini may be go-to carrier to avoid Singapore congestion

-

Carriers may stop calling at some ports in 2025

-

Seek assurances that carriers can deliver what they promise

自2025年2月1日起,在全球六大主要航线——跨大西洋、跨太平洋、亚欧和亚中东航线上,将有三个主要联盟运营:

双子星联盟(Gemini Cooperation) :由马士基和赫伯罗特组成的最新联盟。

海洋联盟(OCEAN Alliance):中远集团、CMA CGM和长荣等航运公司组成的最大航运联盟。它于 2017 年推出,现已确认将持续到 2032 年。

Premier Alliance:由THE Alliance更名而来,该联盟由ONE、HMM和Yang Ming航运公司组成。

值得注意的是,MSC是全球 TEU 运力最大的航运公司,并没有加入上述联盟。这是因为MSC将在2025年采用独立运营策略,并签订了一些舱位共享协议。

“最佳”承运人/联盟的选择在很大程度上取决于发货人的需求,但以下是一些需要考虑的因素:

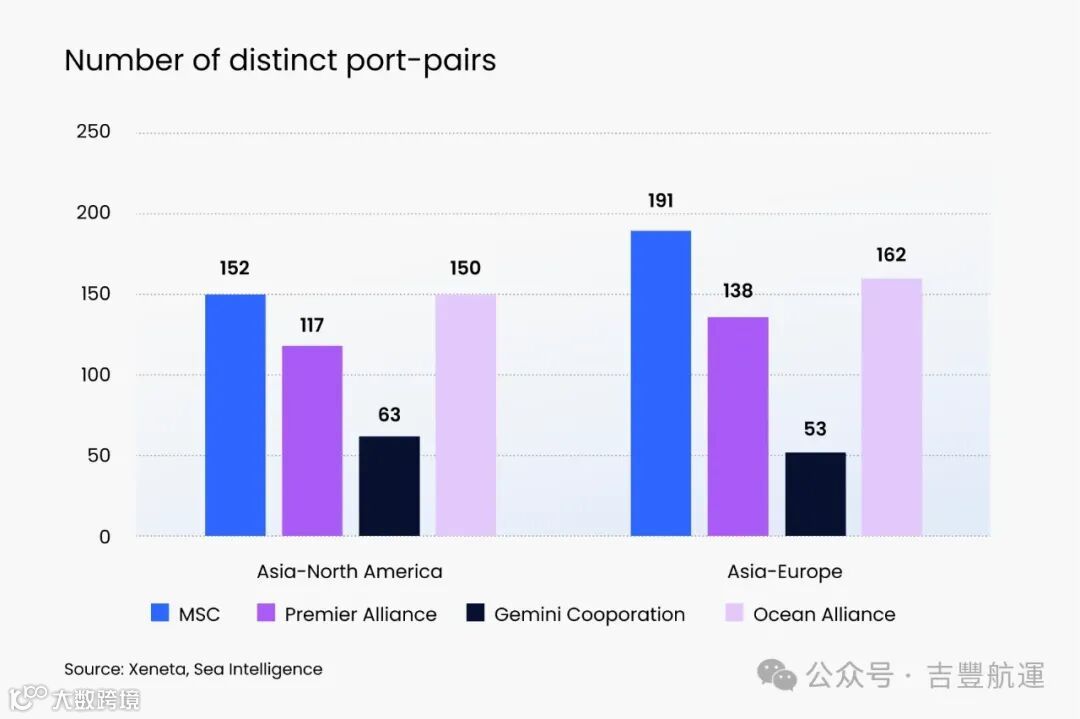

服务数量(循环)

OCEAN Alliance名列前茅,在 6 条主要贸易航线中的 5 条航线上提供最多的服务。它只有在跨大西洋交易中没有占据榜首,仅次于Gemini和 MSC。

运营运力(自有和租赁)

与其他联盟相比,OCEAN联盟将是运力最大的联盟。根据现有的船舶运力数据,它拥有全球运力的28.9%。排名第二的是Gemini,紧随其后的是MSC,而Premier Alliance仅以 11.5% 紧随其后。

As of 1 February 2025, there will be three main alliances operating on the world’s six major fronthaul trades found on Transatlantic, Transpacific, Asia-Middle East and Asia-Europe routes:

Gemini Cooperation – the newest alliance in the market comprising Maersk and Hapag-Lloyd.

OCEAN Alliance - the alliance with the largest group of carriers, consisting of COSCO Group, CMA CGM and Evergreen. Launched in 2017 it has now been confirmed to run until 2032.

Premier Alliance - rebranded from THE Alliance, this carrier partnership consists of ONE, HMM and Yang Ming.

Notable by its absence from the above alliances is MSC – the world’s largest carrier by TEU capacity. That is because MSC is adopting a standalone approach in 2025 with some slot sharing agreements.

The ‘best’ carrier/alliance depends heavily on what a shipper is looking for, but below are some factors to consider:

Number of services (loops)

OCEAN Alliance comes out on top, offering the most services on five out the six major trade lanes. Only on the Transatlantic trades does it not take top spot, sitting behind both Gemini and MSC.

Operated capacity (owned and chartered)

Comparing alliances, the OCEAN Alliance will be the largest by quite a margin. Based on today's fleet it has 28.9% of global capacity. In second place is Gemini closely followed by MSC, while the Premier Alliance trails behind with only 11.5%.

红海冲突导致承运商在非洲各地重新安排服务路线,并无意中导致新加坡的主要港口成为拥堵中心。

如果托运人希望在2025年避开新加坡,他们可能会转向双子星联盟的枢纽辐射模式,服务将在通往欧洲和地中海的前沿的邻近丹戎佩莱帕斯停靠。在回程中,大多数服务将在新加坡停靠,而不是丹戎佩莱帕斯。

相反,MSC 的 7 条服务中有 6 条在新加坡停靠,同时提供前程和回程路线。

Gemini 声称,由于“网络得到改善”,主要航线的运输时间总体缩短,称从上海到鹿特丹只需要32天。MSC 将同一航线的运输时间定为 35-42 天。

这就是MSC与Premier Alliances的舱位互换协议发挥作用的地方,使其能够在运输时间上与Gemini和Ocean Alliance竞争。

如果您要将货物从远东运至安特卫普,那么MSC很可能是您的首选承运商,2025 年每周停靠 4 次。相比之下,Premier Alliance每周停靠1次,而 Gemini 则没有。

托运人的一个关键点是,不要假设您现有的承运商在 2025 年会继续停靠相同的港口。

Xeneta 数据通过对供应商的港口到港口运费、可靠性、运力、运输时间、附加费和二氧化碳排放进行基准测试,支持托运人为其供应链找到合适的承运商。

Limited port calls in Singapore

Conflict in the Red Sea saw carriers re-route services around Africa and inadvertently cause the major transshipment hub of Singapore to become an epicenter for congestion.

If shippers are looking to avoid Singapore in 2025, they may turn to Gemini’s hub and spoke model, with services calling at neighboring Tanjung Pelepas on the fronthaul to Europe and Mediterranean. On the backhaul, most services will stop at Singapore and not Tanjung Pelepas.

Conversely, six out of seven services by MSC stop in Singapore on both fronthaul and backhauls routes.

Transit times

Gemini is claiming overall reduction in transit time on major corridors due to ‘improved network’, citing 32 days from Shanghai to Rotterdam. MSC puts transit time on the same route at 35-42 days.

This is where MSC’s slot swaps with the Premier Alliances come into play, allowing it to compete with Gemini and Ocean Alliance on transit times.

Winners and losers at port level

Shifting alliances will have a big impact at port level.

If you are shipping cargo from the Far East to Antwerp, then MSC is likely to be your preferred supplier with four weekly calls in 2025. This compares to one call a week with Premier Alliance and none from Gemini.

A key point for shippers is to not assume your existing carriers will continue to call at the same ports in 2025.

Xeneta data is supporting shippers in identifying the right provider for their supply chain by benchmarking providers’ port-to-port freight rates, reliability, capacity, transit times, surcharges and CO2 emissions.

承运人和货运代理战略

联盟成员之间的策略变化可以解释为承运人采取了不同的发展路径。以马士基(Maersk)和地中海航运(MSC)为例,两者的策略形成了鲜明对比。马士基致力于成为一个端到端综合物流服务集成商,寻求从长期客户的物流支出中获得更多收益,而MSC则更侧重于现货市场的运营,更关注作为船舶运营商的盈利能力。在MSC收购货运代理公司的同时,它保持这些公司在独立品牌下运营,类似于达飞海运(CMA CGM)对CEVA的策略,而马士基则选择将收购的公司整合在同一品牌之下。这种策略上的差异导致了联盟内部的摩擦,也反映了两家公司在市场定位和业务发展上的不同选择。

托运人应该考虑这些不同的策略,并权衡每个策略的利弊以及它们如何适用于自己的供应链——没有一种解决方案适用于所有情况。货代公司也需要做出自己的决策,但可能会发现与CMA CGM和MSC这样的承运人合作更容易,因为它们在海上运输方面并非直接竞争对手,而马士基正努力成为这样的竞争对手。

货代公司方面也有一些变化,最引人注目的是 DSV 收购了 DB Schenker*,其结果尚不清楚,但就像不断变化的联盟一样,托运人应该对变化保持清醒,并了解如何最好地应对这些变化。

在大型并购之后,新客户总是有机会争取的,这次也不例外,货代公司将竞相争夺市场份额。

注释:在获得监管部门批准并满足条件后,预计将于 2025 年第二季度开始将 Schenker 整合到 DSV 中。

Carrier and freight forwarder strategies

Some of the shifts in alliances can be explained by carriers’ different strategies. Maersk and MSC being a clear example, the former concentrating on becoming an integrator with a heavy exposure to the long term market, contrasting with the latter’s concentration on being a carrier with a higher spot market exposure. While MSC has been buying freight forwarders, it keeps them under a separate brand, much like CMA CGM with CEVA, whereas Maersk is keeping it under the same brand.

Shippers should take these different strategies into account, considering the benefits and disadvantages of each and how they apply to their supply chains – there is no one answer fits all. Freight forwarders also need to make their own decisions – but may well find it easier to work with carriers such as CMA CGM and MSC on the ocean side who are not direct competitors as Maersk is striving to be.

There are also changes on the freight forwarder side, the most notable being DSV’s acquisition of DB Schenker*, the outcome of which is at yet unknown, but just as with shifting alliances, shippers should be awake to the changes and understand how best to react to them.

New customers are always up for grabs following a mega-merger and this time will be no different as freight forwarders compete to gain market share.

Footnote: Integration of Schenker into DSV is expected to begin in Q2-2025 following regulatory approvals and conditions fulfilled.

“托运人必须了解新联盟在他们使用的航线上提供什么——这远不止是价格问题。它涉及到成本、可靠性和运输时间之间的平衡,同时还要意识到,目前使用的承运人可能不是未来的最佳选择。保持选择的开放性,不要害怕挑战承运人,并寻求他们能够兑现承诺的保证,特别是在服务可靠性方面。”

“Shippers must understand what the new alliances are offering on the trades they utilize – and it comes down to far more than price. It is a balance between cost, reliability and transit time, while also being aware the carrier you currently use may not be the best one going forward. Keep your options open, do not be afraid to challenge carriers and seek assurances they can deliver what they are promising, particularly around service reliability.”

5. Disruption: List of risks to manage keeps getting longer

-

-

-

-

-

-

-

-

Supply chains will continue to be impacted by Red Sea conflict in 2025

-

Panama Canal set to be free of drought restrictions

-

Threat of further strikes on US East and Gulf Coast

-

Tariffs on Chinese goods could damage trade

-

Shippers move from just-in-time to just-in-case

-

Freight procurement should not focus solely on cost

-

Prepare for as-yet-unknown disruptions

2024 年,地缘政治和供应链区域争端的威胁已经显而易见,而这些重大中断现在正以越来越频繁和越来越严重的方式发生。托运人应该预料到 2025 年的可能进一步动荡并做好计划。

中东冲突和红海袭击

以色列和哈马斯之间的冲突是胡塞武装袭击红海船只的背景。2025 年该情况改善的希望性很小。

这意味着海运供应链将继续受到影响,不仅在长期和短期运费方面,而且在运输时间、运力限制和拥堵方面。

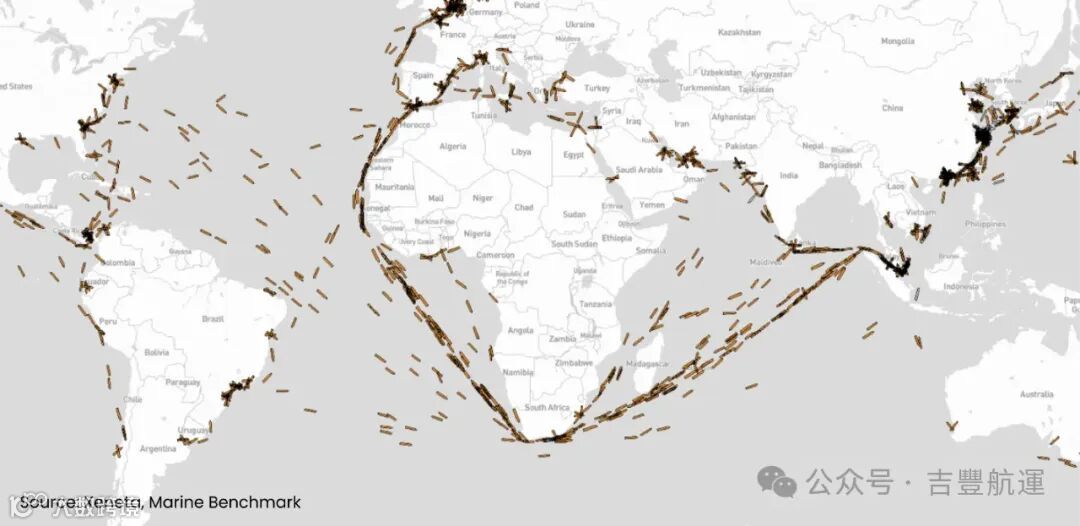

上图显示 2024 年 10 月 8 日,超过 8000 TEU 的船只在好望角附近改道(来源:Xeneta 和 Marine Benchmark)

Image above shows ships over 8 000 TEU diverting around the Cape of Good Hope on 8 October 2024 (source: Xeneta and Marine Benchmark)

巴拿马运河干旱

巴拿马运河在2024年因干旱而面临限制,但情况正在好转。2024年10月7日,加通湖水位达到了86.2英尺,远高于该月份五年平均水平。因此,预计困扰这条重要海上动脉的限制在2025年将不再是问题。这意味着,对于依赖巴拿马运河的航运公司和货主来说,2025年的运营将更加顺畅,不再受到干旱导致的通行限制的影响。随着水位的恢复,这条重要的海上通道将能够更好地服务于全球航运,减少因干旱而引发的运输延误和不确定性。

美国罢工威胁

虽然美国东部和墨西哥湾沿岸的港口罢工在三天后结束,但最终协议尚未签署。新的截止日期为 1 月 15 日,以便进行进一步的谈判,但由于自动化问题仍然是一个备受争议的问题,不能排除在 2025 年可能有进一步的罢工行动。这将与中国新年前的交易量相吻合,这意味着罢工的影响仍然会很严重。

贸易紧张局势和关税

2025 年,白宫的下一任主人将对海运集装箱航运产生重大影响。唐纳德·特朗普(Donald Trump)承诺,如果他成为下一任美国总统,将对中国商品(以及来自世界其他地区的商品)征收更高的关税。

如果特朗普如愿以偿,预计中国将进行关税报复。我们已经看到中国向其他国家出口多元化,包括一些最终进入美国时将用作避免关税的中转站。

为未知做好准备

其他潜在的爆发点威胁着 2025 年的供应链,无论是孟加拉国的政权更迭、台湾海峡的军事行动,还是另一场全球大流行病或气候相关事件。

在 2024 年,许多托运人在其供应链中已从准时转向以防万一,在红海爆发冲突和美国大西洋沿岸受到罢工威胁后,今年早些时候将进口货物提前装载。

托运人应从纯粹关注成本的货运采购策略转变为平衡获得尽可能低的费率和更高的服务水平的采购策略。使用数据将您的业务定位在市场中的适当水平,让您更有可能与您的承运人或货运代理合作,找到一个双方都同意的解决方案,以便在下一个黑天鹅事件到来时保护供应链。

The threat of geo-politics and regional disputes on supply chains has been clear and present during 2024 – and these major disruptions are now happening with increasing frequency and severity. Shippers should expect and plan for further turmoil in 2025.

Conflict in Middle East and Red Sea attacks

Conflict between Israel and Hamas has served as the backdrop to Houthi attacks on ships in the Red Sea. There is little prospect of the situation improving in 2025.

This means ocean supply chains will continue to be impacted, not only in respect of long and short term freight rates, but also transit times, capacity restraints and congestion.

Panama Canal drought

There is better news at the Panama Canal, which has seen restrictions due to drought during 2024. The Gatun Lake water level stood at 86.2 feet on 7 October 2024, which is well above the five-year average for the month. The restrictions which have plagued this vital maritime artery should not be an issue in 2025.

US strike threat

While port strikes on the US East and Gulf Coasts ended after three days, a final agreement has yet to be signed. A new deadline of 15 January has been set to allow further negotiations but with the issue of automation remaining a highly-contention issue, further strike action cannot be ruled out in 2025. This would coincide with pre-Chinese New Year volumes meaning the impact of a strike would still be severe.

Trade tensions and tariffs

The next occupant of the Oval Office will have a big influence on ocean container shipping in 2025. Donald Trump has promised heightened tariffs on Chinese goods (and goods from the rest of the world) should he be the next US President.

Tariff retaliation would then be expected from China should Trump get his way. We are already seeing China diversify its exports to other nations, including some which will be used as a stop to avoid tariffs when eventually moved into the US.

Preparing for the unknown

Other potential flashpoints threaten supply chains in 2025, whether it is regime change in Bangladesh, military action in the Taiwan Strait or even another global pandemic or climate-related incident.

Many shippers have now moved away from just-in-time to just-in-case in their supply chains during 2024, frontloading imports earlier in the year following outbreak of conflict in the Red Sea and threat of strikes on the US Atlantic coasts.

Shippers should move away from freight procurement strategies that focus purely on cost to one which balances getting the lowest possible rate with a higher service level. Using data to position your business at the right level in the market makes it more likely you can work with your carrier or freight forwarder to find a mutually-agreeable solution to protect supply chains when the next black swan event arrives.

“聪明的托运人从新冠大流行中吸取了教训,并正在采用一种新的数据驱动方法来进行货运采购和供应链风险管理。在招标过程中追逐最后一美元可能会迅速适得其反,如果市场陷入动荡,而你的集装箱被优先级更高的货主所取代,他们可能已经通过谈判协商了更高的运费和更好的服务水平。

“随着发货人和服务提供商都在寻找在市场冲击下更好的合作方式,与指数挂钩的合同也越来越受欢迎。世界正处于一个危险的时期,因此管理供应链风险和为最坏的情况做好准备从未像现在这样重要。”

“Smart shippers have learned lessons from the pandemic and are taking a new data-driven approach to freight procurement and supply chain risk management. Chasing the last dollar during tenders can quickly backfire if the market is plunged into turmoil and your containers are rolled in favor of those shippers who have negotiated higher freight rates with better service levels.

“Index-linked contracts are also increasing in popularity as both shippers and service providers look for a better way of working during market shocks. The world is in a perilous period so managing supply chains risk and preparing for worst case scenarios has never been more important.”

6. Decarbonization & environmental regulation

红海冲突将继续通过更长的航行距离影响排放

欧盟碳排放交易体系将在2025年扩大覆盖70%的二氧化碳

欧盟ETS附加费受红海改道贸易风险影响

到2025年交付的60%的运力具有替代燃料能力

到2025年交付的运力中有43%将能够使用液化天然气航行

前10大承运商中只有两家不会有任何使用替代燃料的新船

寻求运营商能够兑现承诺的保证

-

Red Sea conflict will continue to impact emissions through longer sailing distances

-

EU ETS ramps up in 2025 to cover 70% of CO2

-

EU ETS surcharges impacted by trade exposure to Red Sea diversions

-

60% of capacity to be delivered in 2025 has alternative fuel capability

-

43% of the capacity to be delivered in 2025 will be able to sail on LNG

-

Only two of the top 10 carriers will not have any new ships with alternative fuel

-

Seek assurances that carriers can deliver what they promise

由于红海改道导致航程延长,在2024年全球碳排放量大幅增加。例如,在远东至地中海前线,与12个月前相比,今年第三季度每吨货物的碳排放量(根据 Xeneta 碳排放指数衡量)增长了60.1%。

国际海事组织 (IMO)继续推动航运行实现其在 2023 年商定的目标,即到 2030 年将碳排放量减少 40%,到 2040 年减少 70%,到 2050 年左右实现净零排放。这些措施包括降低船舶燃料的温室气体强度和对温室气体排放征收全球税。IMO 已将这两点的法规设定为 2025 年秋季之前设立和通过,尽管它们要到 2027 年才能生效。

全球温室气体排放税将降低更便宜的化石燃料和更环保的替代品之间的价格差异。

欧盟 ETS 附加费

随着航运在2025年越来越多地纳入该计划,承运商将不得不为该计划涵盖的70% 碳排放量购买配额,高于2024年的40%,因此托运人应该预料到这一点将反映在更高的欧盟ETS附加费中。

欧盟碳排放配额(EUA)的价格目前为每份配额72.2美元,与年初的价格几乎持平,每份配额覆盖1吨二氧化碳排放。

红海对附加费的影响

从远东到欧洲(受红海冲突严重影响的贸易),欧盟ETS长期费率的平均附加费与年初相比增加了约 25%,进入北欧的每个FEU高达60美元,进入地中海的每个FEU高达49美元。

从地中海到远东的回程增长幅度更大,增长了75%,达到每FEU 35美元。

相比之下,从北欧到美国东海岸和南美东海岸的跨大西洋贸易(在运营上不受红海冲突的影响)的长期费率平均附加费分别下降了约11%至每FEU 58 美元和46美元。

密切关注EUA的价格发展将有助于了解附加费将如何发展。对于受红海影响贸易的托运人来说,任何大规模的退货也应该会降低欧盟 ETS 附加费,以及更普遍地降低燃油附加费。

承运商对新船队燃料能力选择了不同的方式

计划在2025年交付的运力中,近四分之三具有某种形式的替代燃料能力,或者以相对容易地转换为替代燃料的方式建造。

计划交付的运力中有43%(约83万TEU)将能够使用液化天然气(LNG)作为燃料。这一数字明显高于没有额外替代燃料选项的51.3万TEU新加入船队。同时,能够使用甲醇作为燃料的船舶在新运力中也占据了相当大的比例,达到了37.3万TEU。

在前十大承运人中,只有两家不会有任何采用某种替代燃料的新船,它们是长荣海运(Evergreen)和东方海外(OOCL)。

其他承运人在2025年大致分为两类:一类是新船能够使用甲醇作为燃料的,包括中远海运(COSCO)、现代商船(HMM)和马士基(Maersk);另一类是新船能够使用液化天然气(LNG)作为燃料的,包括赫伯罗特(Hapag-Lloyd)和地中海航运(MSC)。

需要注意的是,尽管这些船舶能够使用替代燃料类型航行,但它们也能够使用传统的船用燃料油。

Xeneta的数据使托运人能够在全球主要航线上对承运人的二氧化碳排放绩效进行基准比较,这意味着他们可以在采购策略中同时考虑排放、成本和可靠性。

Longer sailing distances due to diversions in the Red Sea have seen a massive increase in emissions globally in 2024. For example, on the Far East to Mediterranean frontal, emissions per tonne of cargo (as measured by Xeneta Carbon Emissions Index) was up 60.1% in Q3 this year compared to 12 months ago.

The International Maritime Organization (IMO) continues to push the industry towards the targets it agreed in 2023 to reduce carbon emissions 40% by 2030, 70% by 2040 and net zero by around 2050. The measures include reducing the GHG intensity of ship fuel and a global levy on GHG emissions. The IMO has set a deadline for regulation on both these points to be defined and adopted by the Autumn of 2025, though they will only come into force in 2027.

The global levy on GHG emissions would lower the price difference between cheaper fossil fuels and greener alternatives.

EU ETS surcharges

As shipping’s inclusion in the scheme ramps up in 2025, carriers will have to buy allowances for 70% of emissions covered by the scheme on sailings to/from/within Europe, up from 40% in 2024 - so shippers should expect to see this reflected in higher EU ETS surcharges.

The price for EU allowancces (EUA) stands at USD 72.2 per allowance, almost the same as it was at the start of the year. Each allowance covers 1 tonne of CO2 emissions.

Impact of Red Sea on surcharges

From the Far East to Europe – a trade heavily impacted by the Red Sea conflict - the average EU ETS surcharge on long term rates has increased by around 25% compared to the start of the year, up to USD 60 per FEU into North Europe and USD 49 into the Mediterranean.

An even bigger increase can be found on the backhaul from the Mediterranean to the Far East, up by 75% to USD 35 per FEU.

In contrast, the Transatlantic trades from North Europe to the US East Coast and South American East Coast – which are not operationally impacted by the Red Sea conflict – have seen average surcharges on long term rates fall by around 11% to USD 58 per FEU and USD 46 respectively.

Keeping an eye on the EUAs price development will provide some insight into how the surcharges will develop. For shippers on Red Sea impacted trades, any large-scale return should also lower EU ETS surcharges, as well as lower fuel surcharges more generally.

New fleet has split approach to fuel capability

Almost three quarters of the capacity scheduled to be delivered in 2025 has some form of alternative fuel capability, or is built in such a way that that a conversion to alternative fuel can be done relatively easily.

43% of the capacity scheduled to be delivered (830 300 TEU) will be able to sail on LNG. This is considerably more than the 513 000 TEU entering the fleet with no additional alternative fuel options. Methanol capable ships also make up a considerable share of new capacity at 373 000 TEU.

Only two of the top 10 carriers will not have any new ships with some form of alternative fuel. These are Evergreen and OOCL.

Otherwise, carriers are broadly split in 2025 between those whose ships will be methanol capable - including COSCO, HMM and Maersk - and those whose new ships will be able to sail on LNG - including Hapag-Lloyd and MSC.

It’s important to note that while these ships will be able to sail on an alternative fuel type, they will also be able to use traditional bunker fuels.

Xeneta data allows shippers to benchmark carriers CO2 performance across the world’s major trades, meaning they can factor emissions as well as cost and reliability in their procurement strategy.

艾米丽·斯托斯博尔 Emily Stausbøll

Senior Shipping Analyst, Xeneta

“在碳排放问题上,我们只有一条道路可走,那就是减少排放,托运人必须面对不断增加的附加费用这一现实。话虽如此,托运人仍需深入了解他们所选服务提供商的碳排放策略,并勇于质疑任何加在他们总运费中的附加费用。

“即使欧盟排放交易体系在 2025 年提高到覆盖 70% 的二氧化碳排放量,其影响与我们在 2024 年因红海冲突而看到的螺旋式上升的运费相比,也显得微不足道。

“航运业共同承担着迈向零碳排放的责任,但在2024年的混乱中,这一目标似乎已不再是首要任务。如果2025年市场能够恢复平静,我们可能会看到碳减排被赋予更高的优先级。”

“There is only one direction of travel when it comes to carbon emissions and shippers need to face the reality of increasing surcharges. That being said, shippers must still understand the carbon emissions strategy of their chosen service provider and not be afraid to question any surcharge that is added to their all-in freight rate.

“Even when the EU ETS ramps up to cover 70% of emissions in 2025, the impact will pale in comparison to the spiraling freight rates we have seen during 2024 due to the Red Sea conflict.

“The industry has a collective responsibility to work towards net zero, but it seems it has become less of a priority during the chaos of 2024 – perhaps if 2025 brings calmer waters to the market we will see carbon reduction given a higher priority.”