Styrene Industry Integration Progress Accelerated

At the end of the 13th Five Year Plan period, newly added styrene capacity began to be put into production, and the capacity expansion accelerated significantly entering the 14th Five Year Plan period. The industry's capacity growth rate exceeded 24% in 2021, and it may continue to increase in 2022. Under the background of rapid capacity expansion of the industry, the proportion of integrated units has also increased.

With the advantage of saving cost and reducing consumption, Refining and chemical integration has become an important means for enterprises to improve economic efficiency and market competitiveness. At the same time, with the extension of the refining chain, the economic efficiency and environmental protection efficiency of enterprises have been greatly improved. How is the development progress of styrene integration?

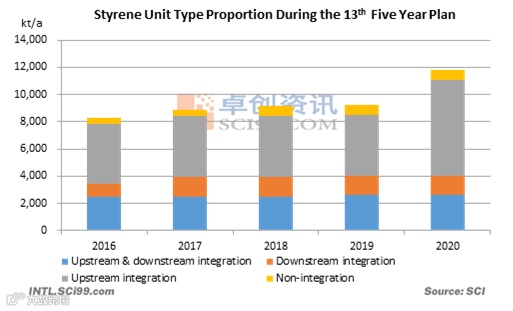

During the 13th Five Year Plan period, the proportion of styrene upstream integration units increased significantly.

During the 13th Five Year Plan period, the capacity of styrene upstream integration units increased significantly, and the capacity of upstream & downstream integration and downstream integration units increased only slightly. By the end of the 13th Five Year Plan, the proportion of styrene integration (including upstream & downstream integration, upstream integration and downstream integration) units had reached 93.72%, and the proportion of non-integration units was only 6.28%. Among them, the proportion of upstream integration units increased most significantly, and the capacity increased from 4,372 kt/a in 2016 to 7,057 kt/a in 2021, an increase of 61.41%.

During the 14th Five Year Plan period, the capacity of styrene upstream & downstream integration units may double.

During the 14th Five Year Plan period, the capacity of styrene industry expanded rapidly. At the end of the 14th Five Year Plan period, the total capacity of the industry may reach 29 million mt/a, twice that at the end of the 13th Five Year Plan. As the largest vertical extension direction of the industrial chain, the capacity of upstream & downstream integration units is expected to reach 5,400 kt/a in 2025, double that in 2020, accounting for 18.64% of the industry’s total.

Remarks: regardless of whether the upstream feedstock of a unit is completely self-supplied or not, as long as there are upstream feedstock or downstream products, it belongs to an integration unit.

All information provided by SCI is for reference only, which shall not be reproduced without permission.

Please click "Read more" for the full article.