2024 China PP Price Runs Counter to Traditional Seasonality

Highlights: China’s PP market prices grew at first but then fell from January to October 2024. As of end-October, the average PP price remained largely steady YOY. The PP mainstream prices fluctuated in a certain corridor at lows, and the fluctuation range shrank YOY. PP prices in some months were against the traditional seasonality. It is predicted that PP market prices may hover at low or trend downwards in the short run. In the long run, oversupply will probably prevail in the PP industry due to the capacity release, and PP prices may stay medium-to-low.

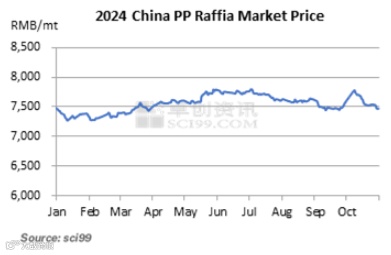

China’s PP market prices grew at first but then fell from January to October. The highest price was RMB 7,795/mt in early July, while the lowest one was RMB 7,265/mt in early-to-mid January. First, China’s PP prices gained ground from January to early July on the back of stronger costs, less-than-expected supply growth and macro-related stimulus policy. Later, higher supply pressure and feedstock cost reduction undermined the PP market price. Although the industry entered the demand peak season from August to September, PP prices continued slipping because the actual downstream stock-up was softer than expectations and the macro environment turned weak. However, market sentiment improved due to the Fed’s interest rate cut and China’s deposit reserve ratio and interest rate reduction at the end of September. The PP futures prices also rebounded, and spot prices also followed that uptrend. As of October, the average price of PP hovered at a past five-year low level, but it rose by 0.34% from 2023.

Ample Supply Pulled Down PP Prices to a Low

In China, PP prices from January to October stood at a medium-to-low level over the past five years, and prices recorded a low in January and September. For the demand side, China’s PP downstream consumption volume grew steadily from 2020 to 2024, but the growth rate was lower than that of supply. In 2024, the total PP consumption volume reached 28,579.5kt by the end of October, up 9% YOY. In the past two years, with the resurgence of tourism and the introduction of consumption promotion policies by the government, PP downstream consumption has been favorable. However, the sluggish infrastructure and real estate industries have limited the improvement of PP consumption. Downstream plants witnessed weakened profits. Large-scale downstream enterprises were more willing to expand plant scale on increasing orders. However, it is difficult for small and medium-scale enterprises to continue to receive plentiful orders and purchase abundant feedstock. Generally, the domestic economy is reviving in 2024, while the overall demand is average. For supply, China’s PP capacity continued expanding from January to October 2024, with fresh capacity of 2,450kt/a. Generally, PP prices hovered at a low because of plentiful supply.

Fiercer Struggle Between Supply and Demand Narrowed PP Price Fluctuation Range

The fluctuation range of PP prices diminished gradually over the past ten years, especially in 2024. Facing oversupply, local PP producers whittled down operating rates sometimes to cope with tepid market demand, which cushioned the price downtrend. Besides, the economic stimulus policy improved the market demand. In addition, PP industry chain profits have slipped in recent years, leading to a cautious stance of players and denting the trading atmosphere. Taking PP raffia as an example, the largest price spread was RMB 530/mt between January and October 2024, which shrank YOY.

2024 PP Prices Broke Traditional Seasonality

According to the PP price characteristics of regularity and seasonality, PP prices usually increase in March, April and Q3 but dropped or lingered at lows in May, June and Q4. September often sees a yearly high, and the middle of a year often encounters an annual low.

In 2024, PP prices in May, June and Q3 were against the traditional seasonality. On the one hand, PP prices went up from May to June, as the extensive maintenance led to supply crunch in Q2 and the introduction of macro policy improved the pessimistic sentiment and weak demand in May. On the other hand, PP prices dropped from July to September, against the traditional trends, mainly as it needs time for the actual effect that policy brings to be seen, and fundamentals performed averagely. Supply moved up because of capacity release, but downstream enterprises showed poor appetite in stockpiling for the upcoming demand peak season, limited by insipid fresh orders from end users. Therefore, the PP industry experienced overwhelming off-season and weak peak season this year, which mainly stemmed from the release of macro policies and changes in fundamental patterns.

Remarks: If PP prices increase, the index is higher than 100%, and if prices decrease, the index is lower than 100%.

From November to December 2024, also 2,450kt/a of PP units are projected to come on stream. The capacity growth rate may rise by 12% YOY, pushing up the overall PP supply pressure. For demand, processors may curtail operating rates given a reduction in new orders, with the demand off-season approaching and temperature decreasing, suggesting falling consumption of PP. Meanwhile, downstream and end users may intend to recoup funds near the end of 2024, which may also restrict their purchases of PP. In the short run, there may be no obvious imbalance between supply and demand, and downstream processors may purchase cheap feedstock, underpinning the PP market somewhat. However, fundamental imbalance may become severe gradually, and PP market prices may drop after narrow fluctuations in the long run, despite that the macro environment may improve due to policy incentives. In December, PP supply may continue to grow, while the downstream demand may stay insipid, weighing down the PP market price continuously. In the future, China’s PP supply and demand will both level up. The growth rate of demand may be lower than that of supply, because the PP demand from traditional fields such as plastic woven and BOPP industries is likely to slow down, but that from automobile and home appliance modification, as well as durable consumer goods will increase strongly, easing some supply pressure and supporting the PP market. PP market prices are likely to rise slightly in 2024, dip narrowly in 2025 but then rebound again in later few years. The overall price level may stay immobile at a medium-to-low level.

All information provided by SCI is for reference only, which shall not be reproduced without permission.

Please click "Read more" for the full article.