玖龍紙業

Nine Dragons Paper Holdings (2689 HK)

漿紙一體紅利持續顯現

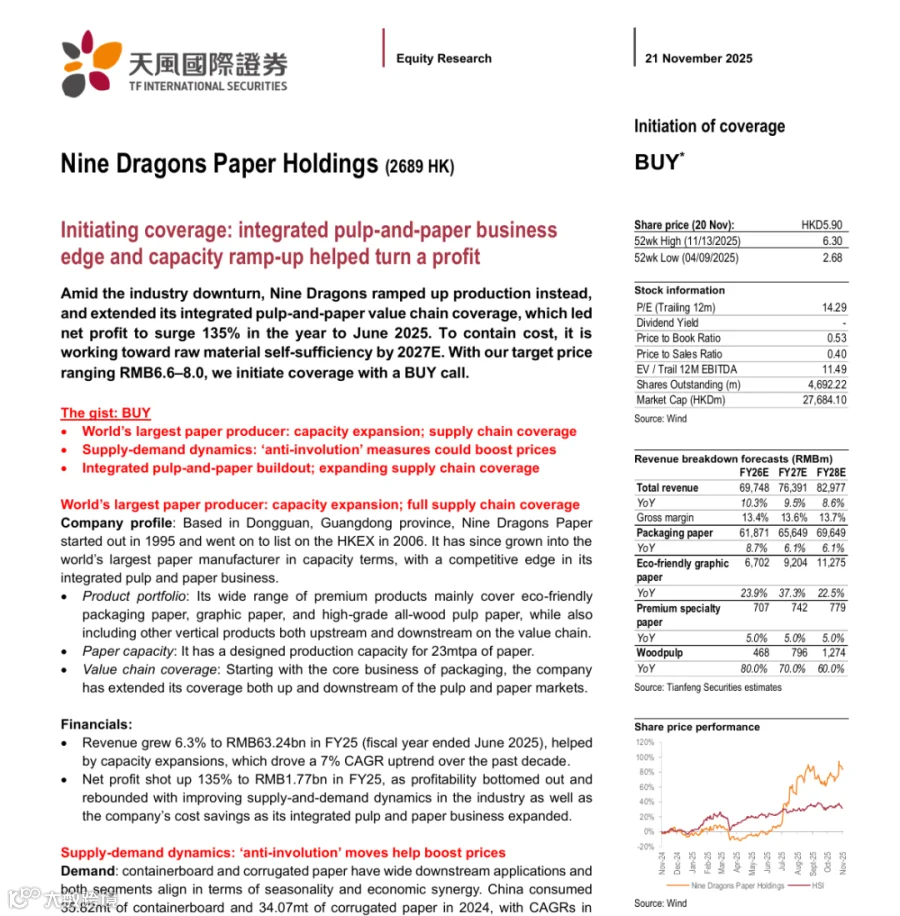

Initiating coverage: integrated pulp-and-paper business edge and capacity ramp-up helped turn a profit

|

買入(首次評級) BUY (Initiation)

|

投資要點/Investment Thesis

投資要點/Investment Thesis

三十年穩步擴張,產業鏈日趨完善

公司成立於1995年,總部位於中國廣東省東莞市,2006年於香港聯交所主板上市,目前為全球產能第一的造紙集團和漿紙一體化的龍頭企業,主要產品為各類環保包裝紙、文化紙、高檔全木漿紙及其上下游產業鏈。 集團現有造紙設計年產能超過2300萬噸,經歷三十年發展,公司從包裝主業向上下游漿紙產業鏈不斷延伸。

近年來產能擴張驅動營收穩步增長,十年收入複合增速達7%,2025財年實現營收632.4億,同比+6.3%; 隨著行業供需格局改善及公司漿紙一體化佈局帶來的成本優化,盈利觸底反彈,2025財年公司實現歸母凈利17.7億,同比大幅增長135%。

箱板瓦楞紙:供需壓力釋緩,反內卷有望提振行情

需求端,箱板瓦楞紙下游應用廣泛,具備季節性、經濟協同性特徵,2024 年我國箱板紙/瓦楞紙消費量分別為3582萬噸/3407萬噸,近五年CAGR為8.3%/7.5%; 隨著國民經濟持續發展,消費品、電商、物流及快遞領域的需求將持續增長,我們預計消費量保持穩定增長態勢。

供給端,從行業產能趨勢來看,2022年以來行業重回產能擴張週期,且禁廢令及零關稅政策推動進口量增加,供需失衡致價格短期承壓。 從目前各公司擴產計劃看,伴隨龍頭新增產能逐漸落地,2025年往後龍頭資本開支收窄,後續產能增量相對有限; 疊加行業價格及盈利低迷環境下龍頭企業規模優勢及成本優勢更為顯著,中小產能陸續出清,我們預計行業供需格局有望逐漸好轉。

短期看,25H2旺季來臨疊加成本上漲推高紙價,我們預計短期價格仍有支撐。 中長期看,行業產能投放逐步回歸理性,此外廣東造紙協會於7月底率先發佈行業第一封「反內卷」倡議書,強調堅決抵制低價無序競爭,主動優化產能結構等,明確行業方向指引,我們認為行業供需矛盾有望逐步緩解,中期價格及盈利有望均值回歸; 後續高質量原材料纖維佈局及成本結構優化或成企業盈利勝負手。

公司:聚焦漿紙一體發展,產業鏈佈局成效顯現

產能規模上,近年公司在行業底部逆勢擴張,截至2025年6月30日,公司造紙及木漿年設計產能接近2900萬噸,FY2022-FY2025造紙新增產能超過500萬噸,產能CAGR達到9%,木漿新增產能超過450萬噸,漿紙擴張節奏基本匹配。 產品結構上,公司堅持豐富拓展高檔牛卡紙、白卡紙等高門檻、高盈利的高端產品,伴隨規模效應顯現,近年噸紙成本下降較為明顯,FY2025噸盈利觸底改善。產業鏈方面,在全面禁廢背景下,公司全力推進漿紙一體建設,我們預計截至25年底,公司將擁有70萬噸再生漿產能、200餘萬噸木纖維產能以及540餘萬噸木漿產能; 未來在重慶、天津、廣西北海等地仍有200萬噸新增木漿產能儲備,預計2027年達到1020萬噸原材料自給能力,有利於最大化降低廢紙採購成本,確保生產質量穩定。

Amid the industry downturn, Nine Dragons ramped up production instead, and extended its integrated pulp-and-paper value chain coverage, which led net profit to surge 135% in the year to June 2025. To contain cost, it is working toward raw material self-sufficiency by 2027E. With our target price ranging RMB6.6–8.0, we initiate coverage with a BUY call.

The gist: BUY

World’s largest paper producer: capacity expansion; supply chain coverage

Supply-demand dynamics: ‘anti-involution’ measures could boost prices

Integrated pulp-and-paper buildout; expanding supply chain coverage

World’s largest paper producer: capacity expansion; full supply chain coverage

Company profile: Based in Dongguan, Guangdong province, Nine Dragons Paper started out in 1995 and went on to list on the HKEX in 2006. It has since grown into the world’s largest paper manufacturer in capacity terms, with a competitive edge in its integrated pulp and paper business.

Product portfolio: Its wide range of premium products mainly cover eco-friendly packaging paper, graphic paper, and high-grade all-wood pulp paper, while also including other vertical products both upstream and downstream on the value chain.

Paper capacity: It has a designed production capacity for 23mtpa of paper.

Value chain coverage: Starting with the core business of packaging, the company has extended its coverage both up and downstream of the pulp and paper markets.

Financials:

Revenue grew 6.3% to RMB63.24bn in FY25 (fiscal year ended June 2025), helped by capacity expansions, which drove a 7% CAGR uptrend over the past decade.

Net profit shot up 135% to RMB1.77bn in FY25, as profitability bottomed out and rebounded with improving supply-and-demand dynamics in the industry as well as the company’s cost savings as its integrated pulp and paper business expanded.

Supply-demand dynamics: ‘anti-involution’ moves help boost prices

Demand: containerboard and corrugated paper have wide downstream applications and both segments align in terms of seasonality and economic synergy. China consumed 35.82mt of containerboard and 34.07mt of corrugated paper in 2024, with CAGRs in containerboard at 8.3% and corrugated paper at 7.5% over the past 5 years. We expect demand will remain stable as the Chinese economy continues to grow, driving demand growth in the consumer goods, ecommerce, logistics and express delivery sectors.

Supply: Industry capacity trends indicate the market has resumed an expansionary cycle from 2022. China’s waste import ban and zero-tariff policies have boosted imports. This led to a supply-demand imbalance, which has exerted downward pressure on prices in the short term. Current expansion plans by companies indicate the new production capacities of leading companies will gradually start to operate. However, with their capex reduced after 2025, any subsequent increase in production capacities will likely be limited. Given currently sluggish industry prices and profitability, with market leaders enjoying scale and cost advantages, it appears that small to medium-sized companies’ production capacities would be phased out. Hence, we believe industry supply and demand dynamics will gradually improve.

‘Anti-involution’ policy shapes healthier market behavior:

Short term: The arrival of the peak season in 25H2, combined with rising costs pushing up paper prices, suggests prices will remain supported over the short term.

Medium to long term: We see industry capacity expansion trends gradually becoming more rational in the longer term. In addition, the Guangdong Paper Industry Association took the lead to issue the industry’s first “anti-involution” initiative at the end of July, expressing firm resistance to self-undermining cut-price competition, and pushing proactive optimization of the market’s capacity structure. This move clearly points to the direction of industry growth. We believe the current misalignment in industry supply and demand will improve gradually, which would lead prices and profits to revert to the mean in the medium term.

Outlook: In the future, we believe that the buildout of a high-quality raw material fiber industry, along with cost structure optimization, could be the decisive factors that determine corporate profitability.

Integrated pulp and paper business buildout; expanding supply chain coverage

Capacity ramp-up: The company has expanded its business against an industry downturn in recent years, with paper and wood pulp production reaching close to 29mtpa in designed capacity. New paper capacity grew by more than 5mtpa at a 9% CAGR over FY22–25, while new woodpulp capacity grew by over 4.5mtpa, keeping pace with paper.

Product mix: Nine Dragons believes in continually optimizing and expanding its product line-up, including high-grade kraft cardboard and white cardboard, premium products that enjoy high barriers to entry and high profitability. As its scale economies come into play, per-ton paper cost has fallen sharply in recent years and led per-ton profit to bottom out and recover in FY25.

Eco-friendly value chain coverage: The company is striving to build up its integrated pulp and paper business amid China’s comprehensive ban on waste imports. We expect its recycled pulp capacity will reach 700kt by the end of 2025, with wood fiber capacity at over 2mt and wood pulp capacity at over 5.4mt. It would then also have additional 2mt wood pulp capacity reserves in Chongqing, Tianjin, and Beihai (Guangxi) cities, among other places. The company expects to achieve self-sufficient raw material capacity at 10.2mt by 2027E, which would go a long way toward reducing waste paper procurement costs as well as ensuring stable production quality.

投資建議/Investment Ideas

首次覆蓋,給予 “買入” 評級

我們預計FY26-28公司歸母凈利潤分別為31.2/34.9/38.4億元,對應PE分別為8.6X/7.7X/7.0X。我們採用相對估值法,公司當前PE及PB處於歷史估值底部,考慮當前公司漿紙一體化穩步推進,預計底部向上週期盈利有望持續改善,此外綜合考慮H股相對A股折價,給予公司26年PE 10X-12X,目標價6.6-8.0元/股,首次覆蓋,給予“買入”評級。

Valuation and risks

We project net profit of RMB3.12bn/3.49bn/3.84bn for FY26/27/28E, which implies 8.6x/7.7x/7.0x PE; relative to peers, Nine Dragons’ current PE and PB ratios are at historical lows. With its integrated pulp and paper business pacing steadily, we anticipate profitability will improve as it trends upward after bottoming out. On top of that, we took into account the relative discount of H-shares to A-shares and assign to Nine Dragons a 2026E PE range of 10x–12x, which derives our RMB6.6–8.0 target price range. We initiate coverage with a BUY rating.

風險提示:原材料價格波動風險,行業供需失衡風險,財務結構惡化風險,政策變動風險,股價波動風險,跨市場選取可比公司估值等風險。

Risks include: raw material price fluctuations; industry supply-demand imbalance; financial structure deterioration; policy changes; share price volatility; and risks related to valuations of cross-market peers.

Email: research@tfisec.com

TFI research report website:

(pls scan the QR code)

本文件由天風國際證券集團有限公司, 天風國際證券與期貨有限公司(證監會中央編號:BAV573)及天風國際資產管理有限公司(證監會中央編號:ASF056)(合稱“天風國際集團”)編制,所載資料可能以若干假設為基礎,僅供作非商業用途及參考之用途,會因經濟、市場及其他情況而隨時更改而毋須另行通知。任何媒體、網站或個人未經授權不得轉載、連結、轉貼或以其他方式複製發表本檔及任何內容。已獲授權者,在使用本檔或任何內容時必須注明稿件來源於天風國際集團,並承諾遵守相關法例及一切使用的國際慣例,不為任何非法目的或以任何非法方式使用本檔,違者將依法追究相關法律責任。本檔所引用之資料或資料可能得自協力廠商,天風國際集團將盡可能確認資料來源之可靠性,但天風國際集團並不對協力廠商所提供資料或資料之準確性負責。且天風國際集團不會就本檔所載任何資料、預測及/或意見的公平性、準確性、時限性、完整性或正確性,以及任何該等預測及/或意見所依據的基準作出任何明文或暗示的保證、陳述、擔保或承諾而負責或承擔任何法律責任。本檔中如有類似前瞻性陳述之內容,此等內容或陳述不得視為對任何將來表現之保證,且應注意實際情況或發展可能與該等陳述有重大落差。本檔並非及不應被視為邀約、招攬、邀請、建議買賣任何投資產品或投資決策之依據,亦不應被詮釋為專業意見。閱覽本文件的人士或在作出任何投資決策前,應完全瞭解其風險以及有關法律、賦稅及會計的特點及後果,並根據個人的情況決定投資是否切合個人的投資目標,以及能否承擔有關風險,必要時應尋求適當的專業意見。投資涉及風險。敬請投資者注意,證券及投資的價值可升亦可跌,過往的表現不一定可以預示日後的表現。在若干國家,傳閱及分派本檔的方式可能受法律或規例所限制。獲取本檔的人士須知悉及遵守該等限制。