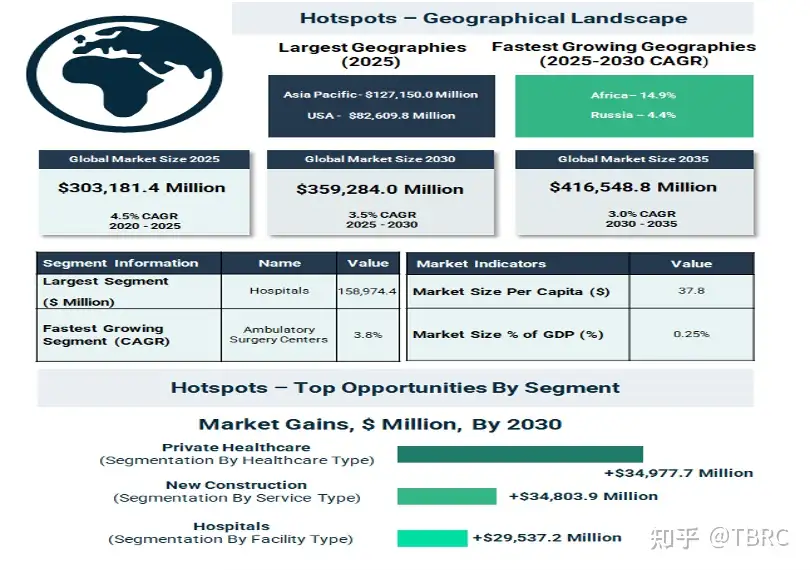

| 2025年市场规模 | $3,031.81亿 |

| 2030年预测规模 | $3,592.84亿 |

| 2035年预测规模 | $4,165.49亿 |

| 2025-2030年复合增长率 | 3.5% |

| 核心驱动因素 | 设施现代化、私营投资、专科照护需求、公私合作 |

| 最大建筑类型 | 医院(52.4%,$1,589.74亿) |

| 最大建设活动 | 新建(63.4%,$1,921.49亿) |

| 最大区域市场 | 亚太(41.9%,$1,271.50亿) |

不只是盖楼,更是重新定义医疗空间

全球医疗体系正在经历结构性变革,这不只是服务模式的变化,更是设施建设和升级方式的变化。患者数量的增长、先进医疗技术的整合和运营效率的提升,都在推动公共和私营部门重新思考医疗基础设施。建设和改造医疗设施已经成为长期医疗规划的核心组成部分。

Healthcare systems across the world are undergoing a structural transformation, not only in how care is delivered but also in how facilities are built and upgraded. The need to accommodate growing patient volumes, integrate advanced medical technologies, and improve operational efficiency is pushing both public and private stakeholders to rethink healthcare infrastructure. As a result, construction and redevelopment of healthcare facilities are becoming central to long-term healthcare planning.

市场在2025年达到$3,031.81亿,到2030年将增至$3,592.84亿,2035年进一步达到$4,165.49亿。这个增长体现了在扩大医疗产能的同时,持续改造存量设施以满足不断提高的照护标准的迫切需求。

The healthcare buildings market reached $303,181.4 million in 2025 and is projected to grow to $359,284.0 million by 2030, eventually reaching $416,548.8 million by 2035. This growth highlights the ongoing need to expand healthcare capacity while modernizing existing facilities to meet evolving standards of care.

过去的根基与未来的动力

早期市场发展受政府医疗支出增长和患者人口扩大的推动。慢性疾病的增加让医疗体系需要更多基础设施来支撑长期治疗和照护。医院、诊所和专科设施的投资在塑造市场增长方面发挥了关键作用。但高昂的资本需求和建设技工短缺在某些地区拖慢了项目执行。

The development of the healthcare buildings market has been strongly influenced by increased government spending on healthcare and the need to support growing patient populations. As chronic diseases became more prevalent, healthcare systems required additional infrastructure to manage long-term treatment and care. Investments in hospitals, clinics, and specialized facilities played a key role in shaping market growth. However, high capital requirements and shortages of skilled construction labor created challenges that slowed project execution in certain regions.

未来的市场将在扩建和改造之间找到平衡。新建医院和诊所继续驱动需求,而老旧设施的翻新改造变得同样重要。私营部门的参与和公私合作模式正在加速基础设施开发。门诊中心和长期照护单元等专科设施的需求上升也在创造新的机会。环境合规要求、建筑材料供应链中断和全球贸易不确定性可能影响项目周期和成本。

Looking ahead, the healthcare buildings market is being shaped by both expansion and transformation. New hospital and clinic construction continues to drive demand, while the renovation of outdated facilities is becoming equally important. Growth is supported by increasing private sector participation and public-private partnership models. In addition, the rising need for specialized care facilities, such as outpatient centers and long-term care units, is creating new opportunities. At the same time, challenges such as environmental compliance requirements, supply chain disruptions for construction materials, and global trade uncertainties may impact project timelines and costs.

设计趋势与细分洞察

医疗建筑市场正在向更具韧性、更高效、更以患者为中心的基础设施转变。现代设施在设计上更注重灵活性、技术整合和患者体验。模块化建造技术用于重症监护单元、下一代医院以患者为中心进行设计、数字系统提升运营效率——这些都是重要趋势。政府推动的医疗记录数字化也在影响建筑设计,让更互联、更数据驱动的照护环境成为可能。

The healthcare buildings market is witnessing a shift toward more resilient, efficient, and patient-focused infrastructure. Modern facilities are being designed to support flexibility, technology integration, and improved patient outcomes. Key trends include the adoption of modular construction techniques for critical care units, development of next-generation hospitals focused on patient-centric design, and increasing use of digital systems to enhance operational efficiency. Government-led initiatives to digitize medical records are also influencing building design, enabling more connected and data-driven care environments.

从建筑类型看,医院以52.4%的份额($1,589.74亿)稳居最大细分。门诊手术中心增速更快,门诊照护模式因其成本效率和便利性正在获得青睐。新建项目以63.4%的份额($1,921.49亿)主导市场,但翻新改造增长更快——老旧建筑的效率、安全和患者体验改善需求是推动力。私营医疗设施以64.6%的份额($1,957.16亿)领先,但公共医疗增长更快,政府持续扩大医疗可及性和投资大型基建项目。

Hospitals remain the largest segment in the healthcare buildings market, accounting for 52.4% or $158,974.4 million in 2025. However, ambulatory surgery centers are expected to grow at a faster pace, reflecting a shift toward outpatient care models. New construction continues to dominate the market, contributing 63.4% or $192,149.1 million in 2025. At the same time, refurbishment is gaining importance as healthcare providers upgrade existing facilities. This segment is expected to grow faster. Private healthcare facilities account for 64.6% or $195,716.2 million in 2025. Public healthcare is expected to grow at a faster rate, as governments continue to expand access to healthcare and invest in large-scale infrastructure projects.

区域格局与竞争态势

亚太以41.9%的份额($1,271.50亿)领跑,大规模基础设施开发是根基。北美和西欧凭借成熟的医疗体系保持强势。非洲以14.9%的年复合增长率成为增速最快的地区,医疗可及性投资在增加。中东以6.5%的增速紧随其后,政府计划是推动力。东欧和南美随医疗基础设施持续发展保持稳步增长。

Asia Pacific leads the market with 41.9% or $127,150.0 million in 2025, driven by large-scale infrastructure development. North America and Western Europe maintain strong positions due to established healthcare systems. Africa is expected to grow at the fastest rate with a CAGR of 14.9%, reflecting increasing investments in healthcare access. The Middle East is also expanding rapidly with a CAGR of 6.5%, supported by government initiatives. Eastern Europe and South America are showing steady growth as healthcare infrastructure continues to develop.

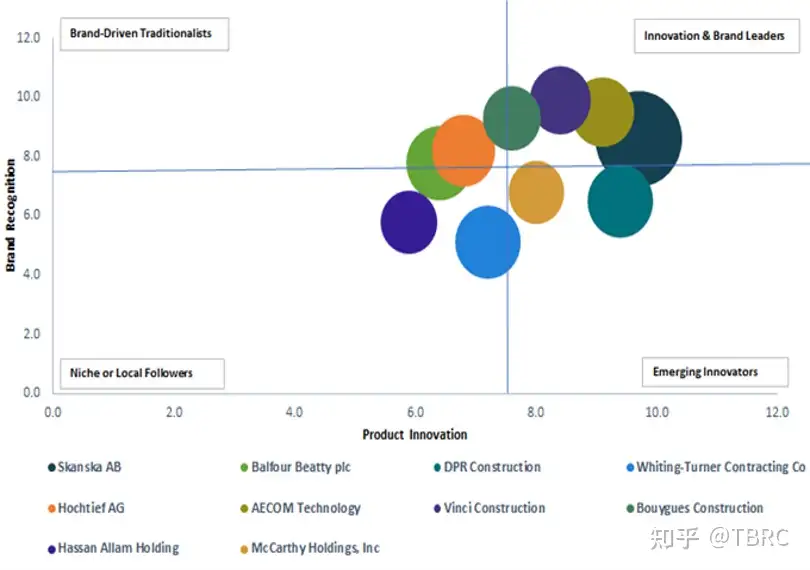

Skanska、Balfour Beatty、DPR Construction、Whiting-Turner、Hochtief、AECOM、Vinci Construction、Bouygues Construction、Hassan Allam Holding和McCarthy Holdings是全球医疗建筑市场的主要参与者。医院、新建项目和私营医疗设施到2030年将产生最大的增量收入。中国以$69.21亿的增量成为最大的市场增长贡献国。企业正聚焦基础设施升级、新项目开发和数字技术整合,模块化建造、先进医疗设施设计和数字系统整合是重点方向。

Key players include Skanska AB, Balfour Beatty plc, DPR Construction, Whiting-Turner Contracting Co., Hochtief AG, AECOM Technology, Vinci Construction, Bouygues Construction, Hassan Allam Holding, and McCarthy Holdings, Inc. Significant growth opportunities are emerging in segments that combine scale and demand. Hospitals, new construction projects, and private healthcare facilities are expected to generate the largest gains by 2030. China is projected to contribute the highest increase in market value, adding $6,921.0 million. Companies in the healthcare buildings market are focusing on strengthening their capabilities through infrastructure upgrades, new project development, and technology integration, with increasing emphasis on modular construction, advanced medical facility design, and digital systems integration.

总结与展望

医疗建筑市场在设施现代化、私营投资扩张和专科照护需求增长的多重推动下稳步前行。随着设计理念和技术持续演进,这个市场将在提升全球医疗可及性和照护质量方面发挥越来越重要的作用。从新建到翻新、从医院到门诊中心,医疗基础设施的每一次升级都在为更好的照护体验铺路。

The healthcare buildings market is steadily advancing under the combined push of facility modernization, private investment expansion, and growing specialized care needs. As design concepts and technology continue to evolve, this market will play an increasingly important role in improving global healthcare access and care quality. From new construction to refurbishment, from hospitals to outpatient centers, every upgrade in healthcare infrastructure paves the way for better care experiences.

数据来源:The Business Research Company (TBRC) |http://www.thebusinessresearchcompany.com

关于The Business Research Company

The Business Research Company (TBRC)是一家领先的市场情报公司,在企业、市场与消费者研究领域享有盛誉。我们已发布超过17,500份报告,覆盖27个行业与60多个地区。我们的研究基于1,500,000个数据集、广泛的二手研究以及对行业领袖的独家访谈。

我们通过市场进入研究包、竞争对手追踪包、供应商与经销商包等专项服务,提供持续及定制化研究支持。

https://www.thebusinessresearchcompany.com