Review

As mentioned above, the most satisfactory part of Ren Bridge this year is that it has demonstrated exceptional resilience. We didn’t even know why we were wrong back in the third quarter of 2023, and then we conducted thorough reflection end of 2023, gradually adjusted ourselves in the second quarter and got on the right track in the fourth quarter this year. It took us one year to complete all the adjustment. Bystanders unfamiliar with the details may not see the struggles and adjustments behind the scenes throughout the calendar year. It is only ourselves that are well aware of the mixed feelings. In terms of returns this year, internet and non-banking financial are the top contributors. Internet was our most favored sector in last year's investment memorandum, and we have already elaborated on the logics. As for the non-banking financial, that is, brokers and insurers, it was our largest exposure before the end of September when the market paid little attention to and barely got involved in the sector, and many friends have once expressed their confusion and concern on this. However, after the policy pivot in September, the upside of the non-banking financial sector was self-evident. At the same time, with the activation of the stock market, brokers and insurers see rapid earnings growth with the fastest and most obvious changes in fundamentals among all sectors, achieving resonance between stock price and earnings. In short, this is a typical case of contrarian investment in traditional cyclicals, same as our previous investments in shipping, aquaculture, oil, agricultural chemicals, non-ferrous metals and electricity. Of course, the violent surge after the end of September was beyond our expectations. Therefore, to be honest, luck must have played a part. However, luck herein lies more in timing rather than direction.

All in all, I want to deliver my gratitude to investors who have been with Ren Bridge through turbulent times. I appreciate your trust and support. I have no doubt that no investment strategy is absolutely better than the other, but each strategy will encounter its headwinds. How to safely weather the headwinds or how to minimize the duration of the headwinds determines the long-term performance of the investment strategy. It is a question that all fund managers can never avoid but must confront. Ren Bridge’s answer to this question can be summarized as three points. First, the fund performance during the hard times should not be too bad. If not, the manager would be under huge mental pressure. With the mental breakdown, his actions can be distorted, either to cringe or to take risks. One would be burnt out under extreme stress for a long time. Of course, to avoid awful performance during headwinds, it is essential to stay rational, diversified and forward-looking in investment and be cautious on leverage. Second, it is crucial to stay more focused during challenging times. To be honest, hard times are painful, and it is humans’ instinct to avoid pain. It is more helpful to make choices against this instinct at such time, that is, to put aside the painful results, find out the original problem leading to the mistakes, seek truth from the facts, make objective evaluation and make timely adjustment. To stay focused in pain can enable progress, as one can hardly make progress in good times. Of course, the incentive for the progress is undoubtedly from the passion deep in the heart. Third, it is important to maintain candid communication with investors. It doesn’t matter how you communicate with them, but the goal is to let them understand what has caused the headwinds. Of course, it is understandable if clients choose to leave regardless of the reasons, but those who choose to stay can become your long-term allies. The understanding and trust from them can provide immense encouragement, as we need spiritual strength to overcome our own difficulties. Therefore, I want to once again thank all the friends who have been with Ren Bridge.

Now let’s talk about the two deficiencies of this year.

First, we haven’t made breakthrough in overseas investments. We have mentioned before that overseas investments can enrich sources of returns and reduce portfolio volatility in the long run. However, we have been pretty cautious on investing abroad: on one hand, Chinese assets are still undervalued compared to global assets, indicating that strategically it may not be the best timing; on the other hand, we don’t want to take reckless action, and we would rather wait till we genuinely have the ability to do overseas investments than bet on luck. Therefore, although we have input some research resources and the research team has strengthened coverage and research of overseas stocks since the beginning of 2024, we haven’t made real investments. Of course, we do find some problems or common difficulties during research: the business of some companies is too complex for us to have sufficient grasp and understanding as the Chinese companies; cultural shock does exist, thus we cannot understand some issues or make high-conviction judgement. I think it’s pretty normal to see these problems, as it is a lengthy and complex process to explore the unknown world and it would definitely take some time for Ren Bridge, whose investment style is extremely conservative and distinctive, to learn and get integrated. Looking ahead, our overseas investments will be more targeted. We will start with companies with relatively simple business models and lower requirements for management expertise or companies that have already proven themselves. We will try not to overlook cyclic industries, which has been the area we are good at. Additionally, we will actively seek like-minded partners. We welcome friends with successful experience in overseas investments to join Ren Bridge and guide everyone here to enhance their vision and capabilities more rapidly. In conclusion, despite the challenges ahead in overseas investment, we are full of confidence in the long run.

Second, we suffered loss from the hedging strategy. Our hedging strategy has been aiming to reduce portfolio volatility and improve clients’ holding experience. Although the loss incurred from hedging is acceptable this year given the rally of the market and our portfolio NAV and also hedging is the only way to reduce drawdown given our high exposure, there remains room for optimization. Based on our repetitive deduction, what we need to do most is to better distinguish between "hedging" and "shorting". Although the two share similar form, their treatment and roles differ entirely. We will make some attempts and changes in the future. Furthermore, we are expecting for regulatory relaxation on short-selling mechanisms for individual stocks, which would enable more precise and effective hedging. In fact, hedging strategies have made little progress in China in recently years because there are few hedging tools. In a highly volatile stock market, many investors do need low-volatility strategies to gain absolute returns. The low-volatility strategies in the past mostly relied on fixed income plus. However, as bond returns have lower margin of safety, there is little room for this method. Looking ahead, we could learn from the mature markets to diversify hedging tools while strictly ban naked short-selling. Only in this way can the investments matrix in China be improved and investors’ needs be better met.

Outlook

Despite the coexistence of risks and opportunities, China’s stock market remains promising in 2025. I write the investment memos at the same time every year, but every years feels different to me. The biggest difference between this year and last year is: last year, there were only a few investment opportunities coming to my mind but conviction for each was high; this year is totally different as there are more opportunities we can be bullish on but conviction for each is lower. However, in terms of portfolio set-up, the above difference may have little impact on the portfolio returns. It would be even more advantageous for a diversified portfolio like Ren Bridge.

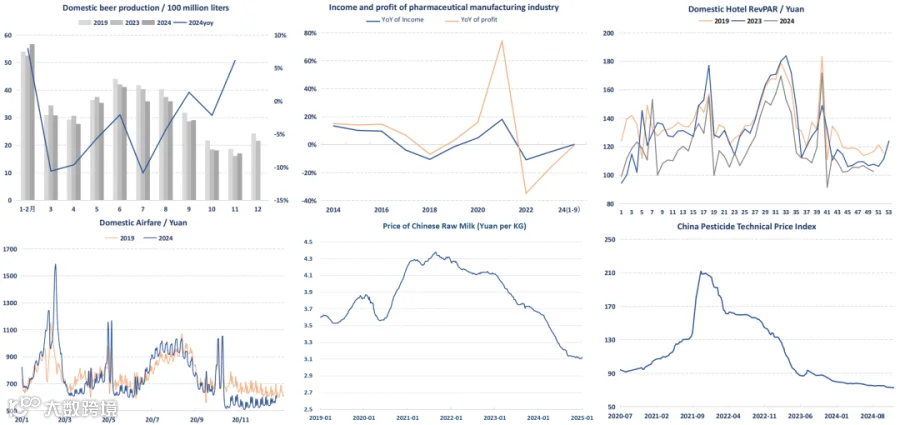

First, we should pay attention to the recovery in domestic consumption. Sectors such as pharmaceuticals, food and beverage, agriculture, airline/lodging/tourism, home furnishings and auto services all hold opportunities.

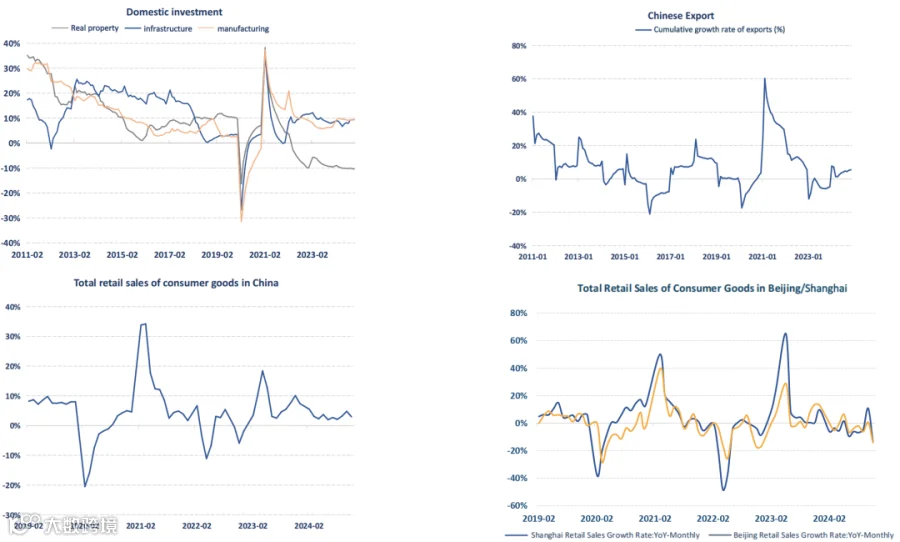

In the three major drivers of the macro economy, consumption should be the most certain and important focus of policies in 2025. On one hand, we have probably already seen the peak of orders and income for infrastructure investment, even though it is not yet evident in the aggregates; real estate investment will continue to hover at the bottom; the manufacturing investment will see pressure coming from the accelerated pace of enterprises going abroad. On the other hand, exports will also face significant uncertainty from U.S. policies, which we can only respond to accordingly. Therefore, boosting domestic demand is the most important way to stabilize economy and the inevitable path of policies in the medium and long run, and the low base of domestic demand across industries in 2024 indeed leaves room for policy implementation.

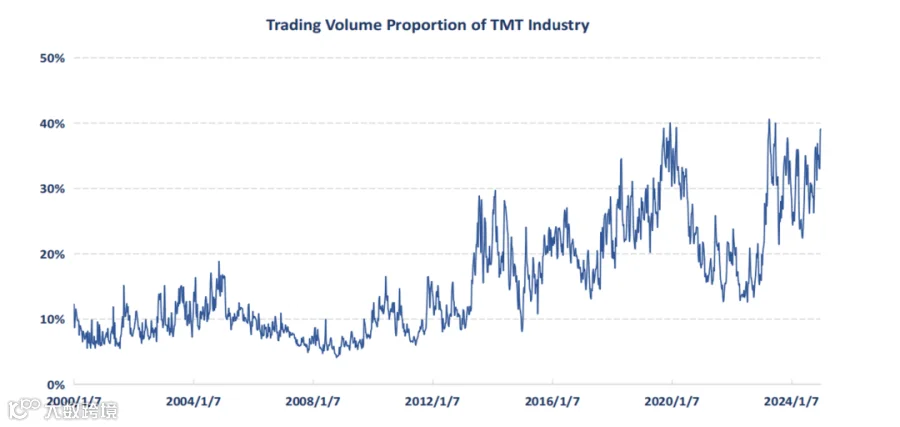

TMT companies will also benefit from the recovery of domestic demand. However, considering most of them have already normalized their earnings over the past two years and their market value has seen considerable recovery, their performance would diverge in 2025. Going forward, we will focus more on their breakthroughs in new technologies and directions, such as the empowerment of AI, as well as their fulfilling of social responsibilities.

Regarding consumption, many may ask, what if there is no more stimulus? Will we follow the suit of Japan where many consumer goods have been declining for many years after peaking such as the apparels industry? Honestly, this question is not easy to answer, although I believe it is unlikely to happen, justified by the differences in per-capita consumption levels and demographic structures between the two countries. Our leading consumer companies do have moats and operational resilience, which at least can be taken as an option. We are most interested in cyclical consumer goods and service consumption with low penetration. In the long run, service consumption still has great potential.

Second, Hong Kong stocks will continue to outperform A-shares, and dividend ETFs the most cost-effective option.

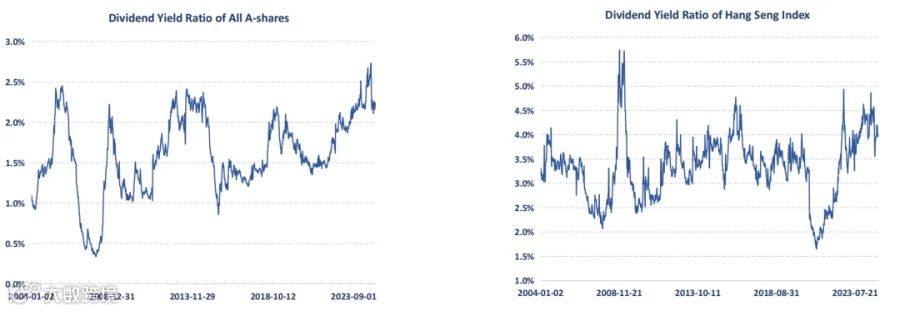

Hong Kong stocks have been lagging behind A-shares since 2019, and they outperformed A-shares in 2024 for the first time. There are many reasons for the rally of Hong Kong stocks, including the U.S. rate cuts, turning around of TMT companies, higher shareholder returns from SOEs, etc. The most important is that Hong Kong stocks are more cost-effective after years’ of retreat. We believe this is a turning point for Hong Kong stocks, and they will continue to outperform A-shares in 2025.

From a long-term investment perspective, we believe that the main contradiction among different assets in China lies in the excessively high risk reward demanded for stocks. The dividend yields of both Hong Kong stocks and A-shares are way higher than the ten-year treasury bond yields, regardless of the possibility that the companies may further enhance dividends and buybacks. Companies that are willing and capable of providing stable and high returns to shareholders will definitely become scarce assets in the future, with their long-term dividend yields expected to approximate the yields of long-term government bonds. This is the only basis for a slow bull market we can imagine and the underlying logic to believe we can continue to gain absolute returns in the future. Of course, this process is bound to be complex and gradual, and we need to be patient and determined. If this logic is eventually confirmed, Hong Kong stocks will naturally continue to outperform.

Lastly, for investors planning on index investing, dividend ETFs , especially those with balanced weightings, are poised to become the most cost-effective ETFs. However, to be honest, the supply of dividend indexes and products is still insufficient, which still has room for optimization and expansion in the future. It may be the next golden track after the A500 index.

Third, bond assets will transit from a one-way bull market to two-way volatility.

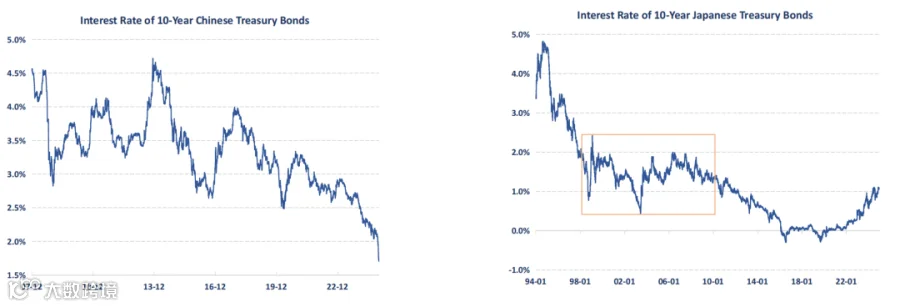

Since 2018, the bond market has enjoyed a six-year one-way bull run. Over this period, China has undergone profound changes. While the stock market has fluctuated, the bond market has consistently demonstrated forward-looking and rational judgment. Bond returns have been the most significant source of investor income during this time. We salute those bond managers who seized historical opportunities to create immense wealth for their clients. However, all financial products are cyclical, and bonds are no exception. Amidst the booming bond bull market, the 10-year government bond yield of 1.7% has rendered this asset class less appealing. As the stock market saying goes, "Don’t chase the last penny”—a principle that may equally apply to current government bonds. This year, the central bank has repeatedly warned of risks, but the market has largely ignored them. This feels like a modern-day "Boy Who Cried Wolf" scenario. Eventually, risks will materialize, and overly aggressive strategies are likely to stumble.

Movements in interest rates are tied to economic conditions. While I believe China will remain in a low-interest-rate environment in the long term, I am more convinced that short-term interest rates will not drop to zero. Future economic cycles, even short ones, will amplify fluctuations in interest rates—this process is inevitable. For instance, in 1990s Japan, interest rates went back and forth for over a decade during their decline and only reached zero after the 2008 financial crisis. While China and Japan differ fundamentally, Japan's experience offers valuable insights into interest rate trends.

Fourth, AI applications will continue to develop, but AI stocks will diverge and speculation will recede.

AI remains a central topic of discussion. Over the past year, the market has displayed a clear investment trajectory, shifting from AI infrastructure to AI applications. Both industry participants and investors have shifted their focus toward the practical applications of AI. We have seen AI+ search, AI+ advertising, AI+ autonomous driving, AI+ education, AI+ healthcare and etc. AI is gradually permeating every aspect of our lives, making it impossible to ignore. We don’t yet know what AI means for humanity in the long term or where it will lead us. For now, we hope its development will benefit humanity, although no one can say for certain. Looking ahead, there’s no doubt that AI capabilities will continue to improve. We have to admit that, since the invention of the calculator, machines have consistently outperformed human brains in certain areas. Thus, developments like Open AI's o3 model surpassing 99% of programmers or achieving competition-level math reasoning no longer come as a surprise—or even excite us. Instead of focusing on cost savings or labor replacement through AI, we are more hopeful about AI’s potential to solve problems or help humanity explore uncharted territories. In this regard, AI+ Autonomous Driving and AI+ Healthcare hold tremendous promise and value, deserving close attention. Looking toward 2025, we anticipate substantial breakthroughs in autonomous driving.

Will the deepening of AI applications drive another surge in AI stocks in 2025? Could it evolve into a full-blown bubble? Honestly, I’ve asked myself these questions repeatedly. I think the answers can be broken down into a few layers: Firstly, a comprehensive bubble similar to the dot-com bubble of 1999 requires many factors to align—industry trends, company performance, liquidity, market style and market sentiment, and these factors must all resonate and amplify each other. Such conditions are rare and represent a low-probability event. Investments should not be based on low-probability assumptions. Secondly, industry development and stock performance can diverge, much like the relationship between economic fundamentals and stock trends. As industries mature and as business models and competitive landscapes become clearer, the stock market will inevitably distinguish the winners from the losers. Those "swimming naked" will eventually be exposed. Lastly, if the low-probability event of an AI bubble does occur, we may underperform despite having some exposure. This outcome—achieving absolute returns but lagging in relative performance—is something I can accept. Once these AI-related questions are clarified, we will have a clearer direction for future actions.

Fifth, inflation is the biggest controversy and a key investment determinant in 2025.

Frankly, very few people can predict the inflation trajectory for 2025 with certainty—and we are no exception. The global inflation outlook has become increasingly unclear since Trump’s rise to power, as many of his policies contain contradictory or offsetting elements. It is challenging to form a confident judgment at this stage. The combination of Trump’s domestic and foreign policies—to conduct reform domestically while to isolate from other countries—lacks historical precedent, leaving us uncertain about their overall impact. We also don’t know whether these policies will be fully implemented or fizzle out halfway. However, one inference seems reasonable: if the U.S. imposes tariffs on other countries as expected, China will likely bear the brunt. In the short term, this would accelerate the relocation of global manufacturing to the U.S., boosting short-term U.S. economic performance. However, it would simultaneously make resolving America’s inflation problem significantly more challenging. From a longer-term perspective, if the U.S. economy experiences cyclical downturns, high manufacturing costs could plunge the economy into a severe and prolonged recession. This is why we outlined in our monthly letter that Trump’s re-election is "pros in the short term while cons in the long term" to the U.S. economy.

From an investment perspective, the trajectory of inflation has clear implications for asset allocation. As inflation is a key factor, how we address it during chaotic periods profoundly impacts final investment outcomes and often serves as a critical determinant of success or failure. At Ren Bridge, our approach to such issues is consistent: we neither ignore them nor take sides. Instead, we focus on option-like assets to optimize investment returns.

In conclusion, in an era of significantly reduced opportunity costs, patience will become the most important driver of returns. Thank you for being with us all the way. After weathering many storms, we remain as youthful as ever. May 2025 bring new growth for Ren Bridge.