China’s central bank has tightened rules on mobile payments made by scanning a barcode, imposing restrictions that could slow the explosive growth for Alibaba’s financial services affiliate and that of its main rival, Tencent.

Daily Limits Payments

The recent regulations set daily limits on the amount consumers can spend each day using QR code payments, which affect venders a lot who receiving money via QR code, and it becomes difficult for consumers to pay a big amount payment via scanning QR code.

New Regulations

■ A single person paying via the static QR code (which are printed and put on walls) has a limit of RMB500 each day.

■ Additional daily limits of RMB 500 for each bank card apply to QR code payers who have connected their bank cards to WeChat Pay.

■ A single person paying via the dynamic QR code (which automatically changes on mobile) has 3 daily limits, RMB1,000, RMB5,000 or they can set an amount for the limit. QR code payers are required to complete different authentication procedures for these 3 limits.

Online Payments Quotas

Quotas of online payments by scanning QR codes vary from person to person according to users’ payment abilities. And there are different levels of “ability verification”. Let's see which type you are!

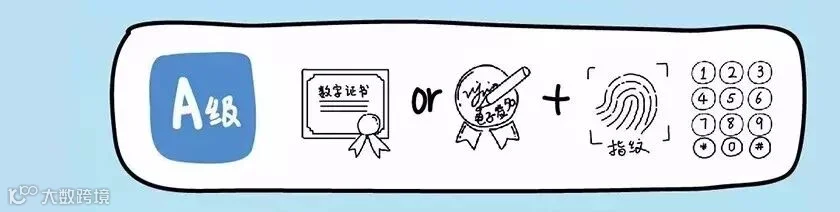

Class A

Online payment account has been verified (at least) by real name and ID numbers with Digital Certificate (CA) and E-signature.

Daily accumulative payment quotas can be decided according to the agreement you make with the financial institution.

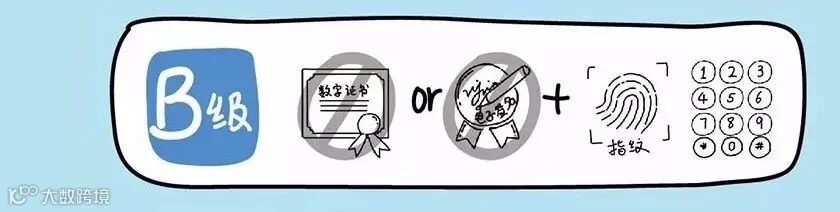

Class B

Online payment account has been verified (at least) by real name and ID numbers but without Digital Certificate (CA) or E-signature.

Daily accumulative payment quotas are no more than RMB5,000.

Class C

Online payment account hasn’t been verified by real name or ID numbers.

Daily accumulative payment quotas are no more than RMB1,000.

Class D

If online payment is made via Static Barcode, daily accumulative payment quotas will be RMB500 of any level of verification.

When to be taken effect?

Alipay and Tencent both issued statements applauding the new regulations, and the new rule will be official taken effect from April 1st, 2018.

China leads the world in mobile payments, most of which are executed by scanning a QR code. While some scans use a specialised point-of-sale (POS) terminal, others occur between mobile phones or when the consumer scans a decal posted near the checkout area.

The value of Chinese third-party mobile payments more than tripled to RMB38 trillion in 2016 and the fast growth continued this year. Alipay, operated by Alibaba’s finance affiliate, Ant Financial, has the largest market share, but WeChat Payment — linked to Tencent’s popular mobile messaging and social media platform — has closed the gap over the past year.

New Rules Target on

Forbidding "Burning Money"

It was said the new rules target on forbidding “burning money” via subsidies to merchants, which are designed to capture market share from competitors.

Since 2014, Alipay and WeChat have spent billions of renminbi on subsidies to merchants and consumers aimed at promoting adoption of their platforms.

But spending on subsidies has slowed since early 2016 as the companies sought to cut expenses, with a decisive victory in the payments war by either side seeming impossible.

QR code payments “have played an active role in promoting financial inclusion”, the People’s Bank of China said in a statement accompanying the new rules. But it also noted that the lack of unified rules and technical standards created “hidden dangers” as well as “improper competition”.

“The market has developed so fast and has become an important payment method, but there are still some technical and market competition problems that need to be brought under control,” said senior analyst at Renmin University’s Chongyang Institute for Financial Studies in Beijing.

Of particular concern is the use of static QR codes such as those posted in shop windows. These codes can be shared, letting unknown parties use them to receive payment.

The People's Bank of China warned that the ability to reproduce and share static QR codes had enabled some payment providers to evade “know your customer” responsibilities by indirectly facilitating payments for merchants with unknown identities.

“In the long run, WeChat Pay and Alipay will benefit,” said Wang Hanyang, fintech payments analyst at 86 Research in Shanghai.

“Fee rates won’t come down, and the price war will probably fade out. Second, more small merchants will switch over” to POS terminals from static codes, locking merchants into the mobile payments ecosystem, he said.

Share to let your friends know!

Source: FinancialTimes

HACOS,Business Services Solutions Master