Shandong is a latecomer when it comes to offshore power generation. However, in the last years, the province has launched an ambitious offshore wind power plan and started exploring innovative offshore power generation technologies. The hoisting of all wind turbines has been completed for the 300 MW offshore wind power project in Changyi. In parallel, the world’s first deep sea floating PV system was grid connected. The project is connected to the grid via a nearby offshore wind platform.

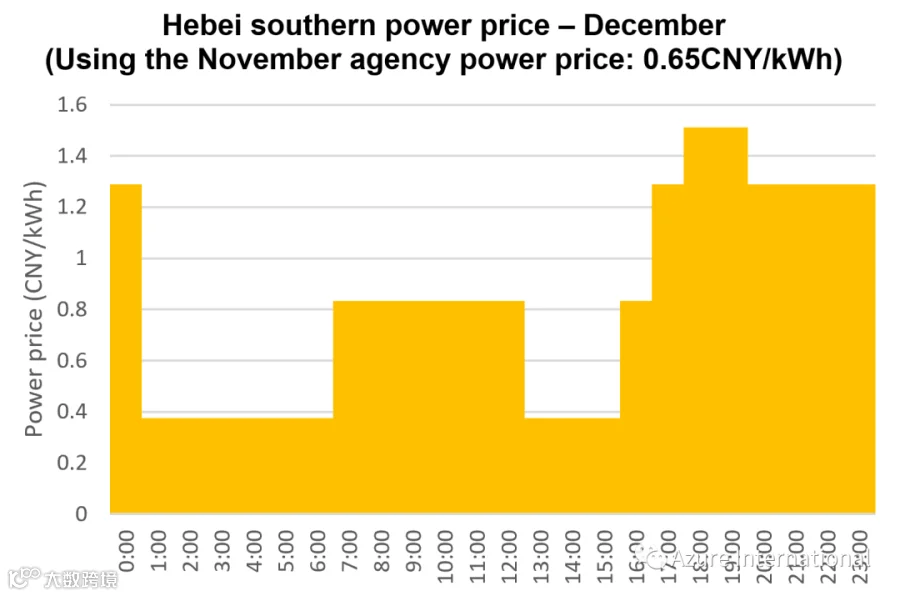

Power stability and security continue to be a challenge for the Chinese grid. Accordingly, the country is taking strong measures to build a more resilient power system. The peak-valley price difference has now reached a considerable 1.1 CNY/kWh in the South Hebei region. This should incentivize power users to increase power consumption during valley hours, when power is cheap, and reduce it during peak hours, when power is expensive. China is also continuing to build up its pumped-hydro storage capacity pipeline. According to incomplete statistics, 43 projects, representing 50 GW in capacity, have made progress towards completion in the last 2 months.

Finally, the Ministry of Ecology and Environment recently released the Carbon Emission Allowance (CEA, which is the Chinese ETS) quota setting and distribution plan for the power industry for 2021 and 2022. Such a document sets the number of free quotas power generators get each year as well as other implementation details. We analyse this document in our Corporate Net Zero Pathways column.

World’s first deep-sea floating PV project launched in Shandong

Turbine hoisting completed at the 3-Gorges Shandong Changyi 300MW offshore wind project

Peak-valley power price difference exceeds 1.1 CNY/kWh in Hebei southern region

China’s pumped hydro sector keeps its momentum as 43 projects make progress in the last 2 months

Corporate Net Zero Pathways: What is new in the Chinese ETS (Carbon Emissions Allowance -CEA) quota setting and distribution plan for 2021 and 2022?

World’s first deep-sea floating PV project launched in Shandong

The 500-kW floating PV demonstration project of Shandong Peninsula South No. 3 offshore wind farm of State Power Investment Corporation(SPIC) successfully generated power last week.

The demonstration project is the first step of the 20MW floating PV farm, which combined with the Shandong Peninsula South No.3 offshore wind farm constitutes the first provincial hybrid renewable project. The clean power generated is merged into the inverter and sent to the Peninsula South No. 3 wind turbine platform operating on the same field. It is then sent to the grid through the offshore booster station.

The project is located in the sea area on the south side of Haiyang City, Shandong Province, 30km offshore and in 30-meter water depths.

Turbine hoisting completed at the 3-Gorges Shandong Changyi 300MW offshore wind project

After four and a half months of intense construction, the hoisting of all 50 wind turbines of the Shandong Changyi Offshore Wind Power Project has recently been completed. The Changyi project is in the northern sea area of Changyi City, Weifang, Shandong.

It has a planned capacity of 300 MW constituted of fifty 6 MW wind turbines. After being put into operation, annual power generation is expected to reach 940 GWh.

Peak-valley power price difference exceeds 1.1 CNY/kWh in South Hebei region

Hebei DRC released the new South Hebei power prices for industrial, commercial, and other users. The policy shows that, shoulder electricity prices are implemented according to the market transaction power purchase price or the grid agency’s average on-grid price.

The electricity price during peak and valley periods will fluctuate up to 70% compared to the shoulder electricity prices. The critical peak electricity price during peak hours will be 20% higher than the peak electricity price.

China’s pumped hydro sector keeps its momentum as 43 projects make progress in the last 2 months

According to incomplete statistics from Polaris Network, 43 projects pumped hydro power stations, representing 50 GW in capacity, have made progress towards completion since September. This includes important steps including approval, start of construction, pre-feasibility study review, etc.

Distributed across 19 provinces, Gansu has been the most active. In the last 2 months, the province has launched the construction of 2 projects (total 2.8 GW), approved 2 projects (2.4 GW), and completed the feasibility study of another 2 (3.2 GW). Back in April, the NDRC and the NEA jointly issued a notice to ‘Accelerate the development and construction of pumped storage projects during the “14thFive-Year Plan” period’, aiming to speed up the approval of pumped storage projects in 2022.

Corporate Net Zero Pathways

What is new in the Chinese ETS (Carbon Emissions Allowance-CEA)quota setting and distribution plan for 2021 and 2022?

A few days before the beginning of COP27, the Chinese Ministry of Ecology and Environment (MEE) released a draft for consultation of the National CEA Quota Setting and Distribution Implementation Plan for 2021 and 2022《2021、2022年度全国碳排放权交易配额总量设定与分配实施方案(征求意见稿)》for the power industry. According to the MEE, the new quota formulation and distribution plan will prioritize energy security and stability of the power generation industry. It will favor sources with high capacity and efficiency, such as CHP, and those engaged in peak regulation. In parallel, the plan also demonstrates a tightening of carbon emissions control.

Quota setting and distribution methodology

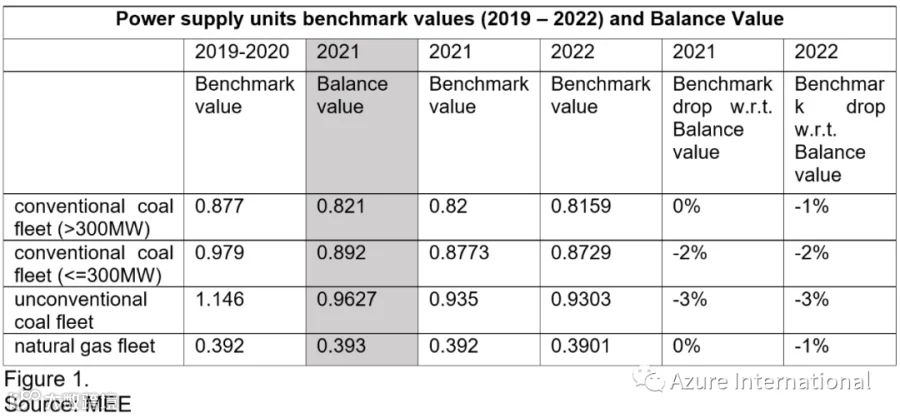

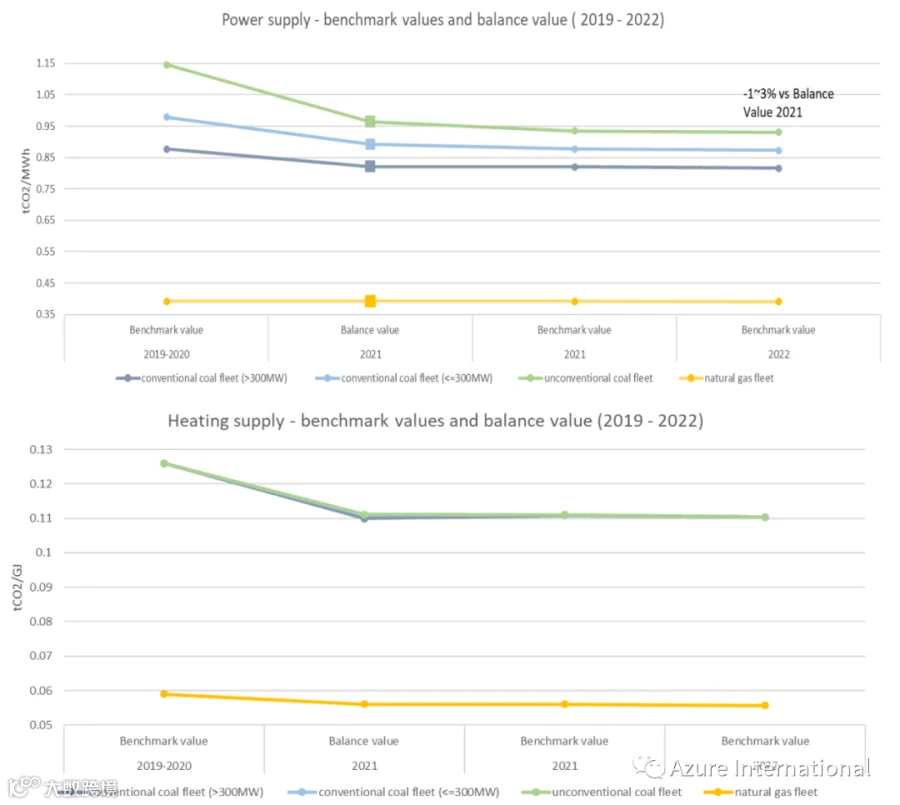

New CEAs will continue to be distributed for free to the key emitters in the power industry. The benchmark value will remain the key indicator for emissions quota calculation for four power generation types:

-

conventional coal fleet >300MW,

-

conventional coal fleet <=300MW,

-

unconventional coal fleet

-

The calculation methodology remains similar to that of the implementation plan for 2019-2020, except that CHP fleets will have more headroom for quota than before, due to the adjustment of the correction factor:

Unit emissions quota = power supply benchmark value × actual power supply amount × correction factor + heating supply benchmark value × actual heat supply amount.

New concept of breakeven balance value is introduced

In the new rules, the concept of breakeven balance value (盈亏平衡值, hereafter Balance Value) is introduced for the first time. The Balance Values refer to the corresponding benchmark values of different unit-types such that their carbon emissions quota is equivalent to their actual emissions. According to the consultative draft, the 2021 balance value is calculated based on the verified emissions of each type of unit in 2021 and the allocation method of the quota determined by the implementation plan, reflecting the actual carbon emission intensity of each type of unit.

Based on the Balance Value, benchmark values of different unit-types will be determined by the regulators, in combination with the carbon intensity reduction targets and other factors.

From the figure 1, we can deduce that the emissions control focus of MEE in 2021 will fall on the conventional coal fleet (<=300MW) and the unconventional coal fleet as their benchmark values (power supply) fall by 2% and 3% against the Balance Values of 2021 while the other two unit-types (conventional coal and natural gas fleet) remain almost intact. In 2022, the focus will shift to the conventional coal fleet (>300MW) and natural gas fleet as the benchmark values go down 1% compared to the actual emissions (Balance Value) in 2021.

The new benchmark values seem much lower than those for 2019-2020, does it mean China will aggressively tighten emissions control?

Compared with the implementation plan for 2019-2020, for which benchmark values were formulated based on theoretical estimations and other factors such as economic growth targets, covid impact, etc, the new benchmark values for 2021-2022 are developed based on the Balance Values which represent the actual emissions intensity. Under such circumstances, it is reasonable to consider the Balance Values as the baseline value of different unit-types. The variation between benchmark values and the Balance Values would point to the emissions reduction gaps emitters will strive to fill. From the depiction 1, the emitters of different unit-types (power supply) will need to reduce emissions intensity by 0-3% respectively in 2021-2022.

In addition, it can be safe to estimate that the emitters should probably have less surplus quota in 2021-2022 than 2019-2020 because the allocation will rely on the actual verified emissions data. It is possible that there will be less quota to be traded in the CEA market for the compliance settlement of 2021- 2022, which will take place at the end of 2023.

(MEE)

This content is prepared by the Research and Strategy Team of Azure International. Please contact us via our official account or email for any enquiry.

E-mail address:

info@azure-international.com

Scan the QR code to follow the official

account of

Azure International Technology

Development (Beijing) Co.,Ltd