Corporate Net Zero Pathways

Energy storage systems bundling requirements for rooftop solar, another policy burden for solar power?

The most common business models for historical C&I (Commercial & Industrial) rooftop solar include:

100% grid-sale

Self-consumed + remainder grid-sale

100% self-consumed

Recent power price spikes are increasing the value of rooftop solar

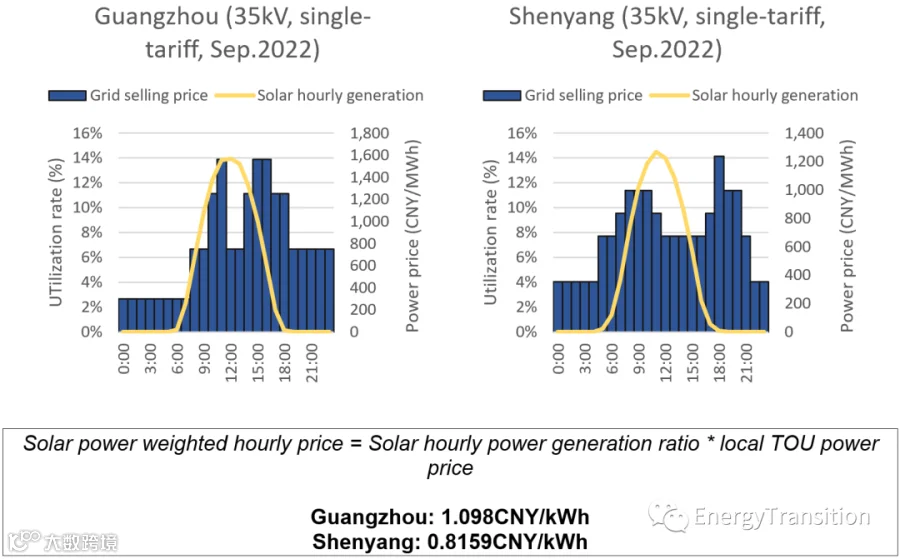

According to the latest grid company power retail prices for September released by the State Grid Corporation of China (SGCC), more than 21 provinces and regions have time-of-use (TOU) gaps larger than 0.7CNY/kWh. Guangdong, Shenzhen, and Shanghai have the most significant gaps, reaching 1.178CNY/kWh, 1.163 CNY/kWh, and 1.397CNY/kWh, respectively.

Would shifting a portion of grid sales to self-consumption make sense?

This is a complicated issue. There are several key elements that need to be considered in the new business model design, such as power user’s load curve, ESCO (Energy Service Company) terms (if any), etc. At the same time, characteristics of different provinces may be determinant too.

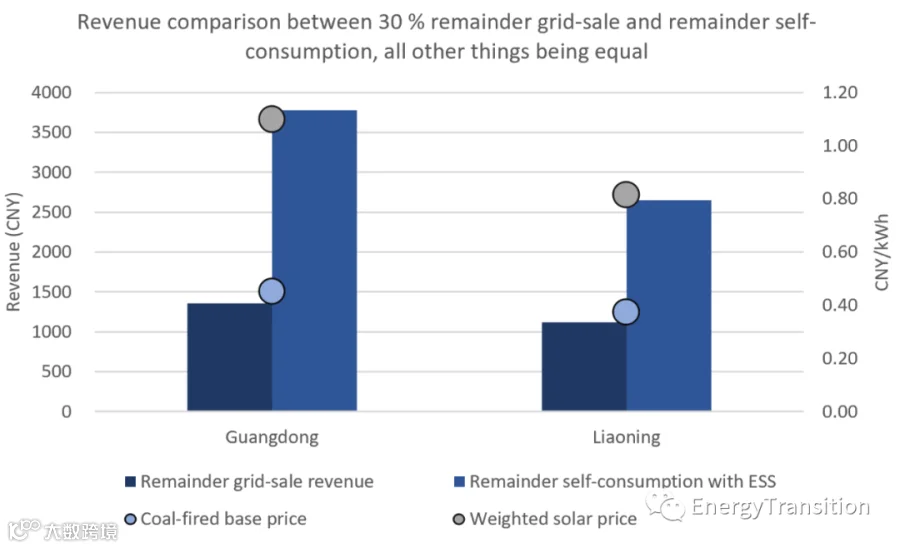

Let’s illustrate this with a dummy example of a rooftop solar project producing 10 MWh annually: 70% of power generation is consumed by the factory who owns the rooftop, the remaining 30% is sold to the local grid company at the local coal-fired base price. The rooftop solar investor is considering shifting the grid-sale portion to self-consumption to monetize the TOU gaps. Supposing the power user could consume all the remaining power at peak hours, let’s compare the scenarios in Guangdong and Liaoning respectively, with all other things being equal (i.e. CAPEX and OPEX, power user’s load demand, and other elements are the same) and TOU price arbitrage is optimized.

Does it still make sense to store the grid-sale portion for TOU arbitrage if peak demand and supply don’t match?

Other business models to create revenues for power user side ESS exist

The evolving power market is enabling a lot more diversified business model for ESS applications, such as Demand Side Response (DSR), peak regulation services through integration of Virtual Power Plants (VPP - certain provinces allow VPP to participate in the peak regulation market), backup power to prevent power crunches, etc.

For instance, the Guangdong DSR implementation plan issued in April this year allows a bidding ceiling of 3500CNY/MWh for the D-1 DSR (day-ahead DSR auction arrangement), and the price for interrupted load demand can reach up to 5000CNY/MWh. Last year, Sinopec Guangzhou earned over CNY 8 million (USD 1.15 million) for 62 hours of DSR services.

Some provincial governments such as Hebei have begun encouraging distributed renewable projects to lease and share the use of independent ESS, which could become a trend in the future. Independent ESS, which is usually at a larger scale, have more flexibility and options to venture in the ancillary services and power spot markets. Shandong has lately issued the first provincial policy to promote independent ESS participation in the power spot market. In addition to a waiver of T&D fees for charging from the grid, the independent ESS of demo projects can also enjoy capacity compensation fees twice that of normal power generators in the power market, which is almost 0.2CNY/kWh!

Scan the QR code to follow

the official account of

Azure International Technology

Development (Beijing ) Co.,Ltd