本文所列价格趋势基于以下2022年全球整体涨幅预估数:机票价格增幅48.5%、酒店价格增幅18.5%以及租车价格增幅7.3%

根据CWT以及全球商务旅行协会 (GBTA) 近日联合发布的2023年度《商务旅行价格趋势》显示,全球差旅业价格将在2022年所剩不多的未来几个月以及2023年持续保持上升态势。

该报告采用了Avrio Institute的评估模型,并以CWT与GBTA双方所提供的已做匿名处理的真实数据并结合了行业公开信息建立了报告统计模型。报告显示,燃油价格上涨、劳工短缺、原材料价格飙升都是导致未来行业价格上涨的关键因素。

数据来源:《2023年商务旅行价格趋势》

“毋庸置疑,商务旅行与会议活动的需求正在全球范围内强劲反弹。”CWT全球首席执行官Patrick Andersen先生认为:“旅游以及住宿业目前出现的劳工短缺,原材料价格上升以及绿色出行话题的行业关注度提升都会对行业产生影响,但我们认为,未来的价格趋势还是会与2019年不相上下。”

“我们看到了多种复合因素都在影响差旅人士与差旅采购所构建的差旅项目。这是第八份联合发布的年度价格预测报告,我们将差旅统计数据、趋势分析与宏观经济因素结合起来, 旨在为企业差旅规划做出前瞻性参考。”GBTA首席执行官Suzanne Neufang女士点评道。

/

宏观经济影响

受新冠疫情冲击,2020年全球经济下滑3.4%,为二战以来最严重的经济衰退。包括旅游业以及住宿业在内的服务业版块饱受重创。但全球经济在2020年后逐步走出低谷,2021年开始回暖反弹,呈现了5.8%的增幅。尽管存在可能再次出现衰退的因素,但全球经济仍在不断企稳回升。根据目前预测,基准场景下,2022年全球经济整体将上涨3%,2023年则增幅2.8%。

《2023年商务旅行价格趋势》中也提及了三大影响经济与商务旅行行业的主要因素:包括俄乌冲突在内的地缘政治风险、通货膨胀导致的价格上涨以及新型冠状肺炎疫情的出现对于商务旅行行业的冲击。

与此同时, 多数企业将可持续性发展列为首要发展,已经显现出应对气候变化的加速重要性。该报告强调了在预定购买的时点,绿色出行选择、碳足迹和环境影响的展示将会成为差旅行业展现企业责任的机会。

/

会议与活动

会议与活动需求因为不确定的经济大环境下得以激增,企业希望构筑更为稳健的内外部文化。因此,各分类价格都有所攀升。2022年,会议与活动单人价格预计较之2021年上升25%,2023年将持续增长7%。

除了以上激增需求。企业会务活动较之2020年大面积取消的状态来看,也呈上升态势。全球来说,很多企业在后疫情时期里,减少了实际办公面积并采用了远程工作的模式。因此,他们对于员工会议线下会务的场地需求大幅增长。

人们对于会议活动的先期准备期也因为后疫情时代不确定因素频发从原先的6-12个月缩短至了1-3个月。这一现象在亚太地区尤为明显,特别中国地区企业客户。由于疫情反复,该地区客户希望能在最短最快时间内确认所有会议活动举办细节。

/

航空

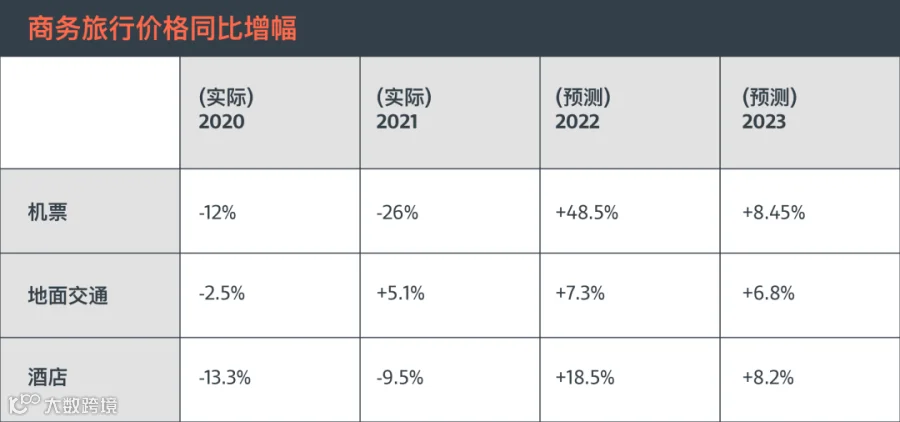

全球商务旅行机票价格于2020年较之上年2019年下跌12%,2021年在此基础上持续下滑26%。经济舱价格从2019年至2021年跌幅24%,头等舱则下跌33%。2022年,预计价格将上涨48.5%,但即便有大幅上涨,机票价格将在全球范围内持续低于疫前水平直至2023年。2023年机票价格将在2022年上涨48.5%的基础上持续上涨8.4%。

根据标准普尔公司 (S&P Global) 数据显示,能源市场紧张,油价上涨,部分市场航空燃料已飙升至160美金/桶的翻倍价格,这无疑将为机票价格带来一定压力。

2019年,头等舱的购买占比约为7%。但2020年下跌至6.5%,2021年持续下滑,跌至4.5%。但2022年起有所回暖。截至上半年,已恢复至6.2%。头等舱的机票份额回升会拉动整体平均机票价格上涨,因为整体平均机票价格包括经济舱和头等舱。

国际机票跨境机票已在很多地区复苏,这将不仅推进国际机票业务也会拉动整体平均机票价格。当然不排除类似俄乌战争的地缘政治事件可能带来的影响。基于过去两年的商务出行支出较少,差旅人士将更愿意在机票上有所支出,特别是劳工短缺的前提下。当然这一趋势的大前提是疫苗普及以及边境开放。

/

酒店

全球酒店价格2020年较之上一年下跌13.3%, 并在此基础上于2021年持续下跌9.5%。但根据报告数字显示,2022年将有18.5%的回升,2023年将在此基础上持续上涨8.2%。在诸如欧洲、中东和非洲以及北美地区,酒店价格已基本恢复至2019年水平。2023年预计全球范围内都能得以恢复至疫前水平。

酒店价格在某些地区得以快速回升:北美上升22%;预计由于需求回暖以及住宿业供给短缺,欧洲以及中东和非洲的价格上涨将飙升至31.8%。

酒店价格的上涨最早是由于2021年私人出行需求暴涨推动的,但企业会议与活动带动的团队游以及商务旅行的恢复也推动了酒店价格上浮。

/

地面交通

全球租车价格2020年较之上一年2019年整体下跌2.5%。2021年则上涨5.1%,2022年有望在此基础上持续上涨7.3%,2023年可能达到增幅新高6.8%。

由于疫情爆发初期,多数租车公司都不约而同减少了车辆与人员,同时由于全球汽车制造业受影响,零部件缺失以及供应链缺乏稳定性,租车行业可能持续面临供给能力限制、尚未全面恢复的困境。

租赁企业可能通过购买二手车或延长车辆使用时间扩充他们的车队。有些甚至可能采购一些不同于现有品牌的车辆以补充车队。

价格上涨、车辆短缺、碳排放考量都会驱使企业差旅负责人将地面交通作为整体出行解决方案的重要一环来部署。例如是否要在未来更多使用电动车,是否要把个人需求考虑在内。

关于《2023全球商务旅行价格趋势》报告

《2023年商务旅行价格趋势》报告基于以下:

-

统计模型由GBTA建立 -

评估模型来自于Avrio Institute对历史价格行为分析并预测航空、酒店和地面交通的未来价格 -

各地市场的专业知识和差旅行业知识来自CWT -

来自国际货币基金组织研究部、IATA、联合国和其他领军机构的信息

预测以CWT全球客户群的交易数据为依据,包括过去十年的客户差旅模式(已匿名处理)。统计模型中使用了关键宏观经济指标和各国指标(例如当前和预计的GDP增长率、消费者物价指数、失业率、原油价格),以及来自OAG和STR Global 的关键供给方驱动因素。所有航空统计数据源自始发地统计,并包括所有旅行类型。

▋ 关于全球商务旅行协会 (GBTA)

全球商务旅行协会 (GBTA) 是全球首屈一指的商务差旅和会议贸易组织,其业务遍及四大洲,总部位于华盛顿特区。GBTA的会员每年管理超过3,450亿美元的全球商务差旅和会议费用。GBTA为28,000多名差旅专业人士和125,000名活跃联系人组成并日益扩大的全球网络提供世界一流的培训、活动、研究、宣传和媒体内容。

▋ 关于CWT

CWT是一家交易量位于全球领先的国际差旅服务商,其经营实体遍及140个国家/地区,品牌历史逾150年。CWT希望藉由差旅管理项目在完善员工出行体验的同时,帮助企业实现差旅成本优化以及人员绩效提升,最终推进企业商业目标并释放无限可能。CWT是首家在华推出开放式API差旅管理平台的B2B4E(面向企业 · 服务员工)国际差旅管理服务商。不仅如此,CWT旗下还拥有专业的会议与活动的专属子品牌,帮助企业实现差旅与会议活动综合管理。

Business travelers set to see air fares rise by 8.4%, hotel rates by 8.2%, and car rental charges by 6.8% in 2023

This is on top of a predicted full year 2022 increase in air fares of 48.5%, hotel rates of 18.5%, and car rental charges of 7.3%

Global travel prices are predicted to continue to increase in the remaining months of 2022 and throughout 2023, according to the 2023 Global Business Travel Forecast, published today by CWT, the B2B4E travel management platform, and the Global Business Travel Association (GBTA), the voice of the global business travel industry.

Rising fuel prices, labor shortages, and inflationary pressures in raw material costs are the primary drivers of the expected price growth, according to the report, which uses anonymized data generated by CWT and GBTA, with publicly available industry information, and econometric and statistical modeling developed by the Avrio Institute.

Source: 2023 Annual Global Business Travel Forecast

"Demand for business travel and meetings is back with a vengeance, of that there is absolutely no doubt," said Patrick Andersen, CWT's Chief Executive Officer. "Labor shortages across the travel and hospitality industry, rising raw material prices, and greater awareness for responsible travel are all having an impact on services, but predicted pricing is, on the whole, on par with 2019."

"What we are seeing now are multiple factors coming into play when corporate travel buyers and procurement officers model their travel programs. This eighth joint annual forecast marries statistical travel data and trend analysis with macroeconomic influences to provide a cornerstone reference point for their corporate business travel planning ahead," said Suzanne Neufang, Chief Executive Officer of GBTA.

/

Macroeconomic influences

The world economy shrank 3.4% in 2020 in one of the worst declines since World War II. Service sectors, including travel and hospitality, were hit especially hard, but the global economy recovered briskly, rising off the lows of 2020 and increasing 5.8% in 2021. Economic growth is moderating as the recovery lengthens, although another recession is a growing concern. The current base case scenario for 2022 is for 3% growth, followed by 2.8% growth in 2023.

Cautionary notes also highlighted in the 2023 Global Business Travel Forecast, highlight the three main forces exerting pressure on the economy and the business travel industry. These include Russia's invasion of Ukraine coupled with other geopolitical uncertainties, inflationary pressures that are pushing costs higher, and the risk of further COVID outbreaks that could restrict business travel.

Conversely, with businesses ranking sustainability among their top priorities and reflecting the accelerated importance of combating climate change, the report highlights greater visibility at the point of sale for greener travel options, as well as carbon foot-printing, and environmental impact assessment is an opportunity for the travel industry to actively assist in responsible choice-making.

/

Meetings and Events

Prices have increased in all regions across most categories of spend, fueled by pent-up demand, a desire to build company culture and an uncertain economic outlook. The cost-per-attendee for meetings and events in 2022 is expected to be around 25% higher than in 2019, and it's forecast to rise a further 7% in 2023.

Alongside pent-up demand, corporate events are now competing with many other types of events that were cancelled in 2020. And, with many companies having given up office space during the pandemic in favor of remote working, they are now booking meeting spaces when staff gather in person, further fueling demand.

Shorter lead times for events, varying from one to three months versus six to 12 months, are also contributing to this perfect storm, perhaps underscored by corporate concerns that the situation they face today could change very rapidly. This is particularly noticeable within Asia Pacific, which has been slower than other regions to re-open post-pandemic, with ongoing restrictions in China prompting clients to make sure their events can go ahead, and as quickly as possible.

/

Air

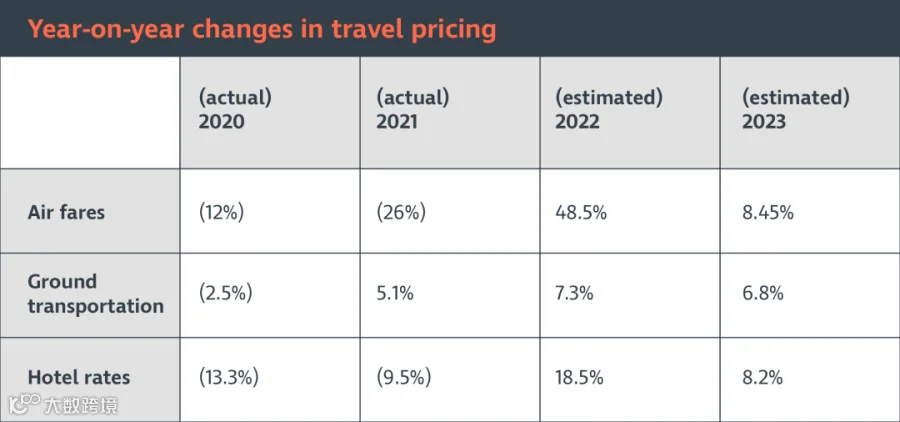

Business travel airfares fell over 12% in 2020 from 2019 followed by an additional 26% decline in 2021. Economy ticket prices fell over 24% from 2019 to 2021, while premium tickets fell 33%. Prices are expected to rise 48.5% in 2022, but even with this steep price increase, prices are expected to remain below pre-pandemic levels until 2023. Following an increase of 48.5% in 2022, prices are expected to rise 8.4% in 2023.

Rising demand and continued price rises on jet fuel, which have seen prices more than double in some markets to over $160/barrel according to S&P Global, are putting upward pressure on ticket prices.

Premium class tickets comprised over 7% of all tickets purchased in 2019. The share of premium class tickets fell to 6.5% in 2020 and to 4.5% in 2021 but have started to rise in 2022. Through the first half of the year, premium tickets made up 6.2% of all tickets purchased. A rising share of premium class tickets will result in higher average fares as average ticket price comprises economy and premium.

International and cross border bookings are recovering across most regions which will result in a higher share of international ticket bookings and a corresponding higher average ticket price despite uncertainties caused by the war in Ukraine. Following two years of minimal to no expenditure, business travelers are likely to be willing to spend more on tickets, especially as availability reduces due to labor shortages. This upward trend is largely due to widespread vaccine rollouts and border re-openings.

/

Hotel

Hotel prices fell 13.3% in 2020 from 2019 and a further 9.5% in 2021, however the report expects them to rise 18.5% in 2022 followed by an 8.2% lift in 2023. Hotel prices have already eclipsed 2019 levels in some areas such as Europe, the Middle East & Africa and North America and are expected do so globally by 2023.

Hotel rates have risen sharply in parts of the world including a 22% rise in North America - and a forecast 31.8% across Europe, the Middle East & Africa - driven by an accelerated recovery coupled with continued capacity constraints.

Hotel rate increases were initially driven by strong leisure travel in 2021 but group travel for corporate meetings and events is improving and transient business travel is similarly gaining healthy pace, putting further pressure on average daily hotel rates.

/

Ground transportation

Global car rental prices fell 2.5% in 2020 from 2019, before rising 5.1% in 2021. Prices are expected to increase 7.3% in 2022, hitting new highs, and rise a further 6.8% in 2023.

The vehicle industry remains capacity constrained and rental agencies which reduced fleet sizes in the wake of the pandemic, have not yet fully recovered - due in part to component shortages and supply chain disruptions that have reduced global auto production.

Rental agencies have reverted to buying used vehicles to increase fleet sizes and are keeping their vehicles longer. Some agencies are also buying vehicles from auto-makers outside of their historically supported brands.

Skyrocketing prices, vehicle shortages and the need for visibility into carbon emissions from door-to-door are driving corporate travel managers to factor ground transport into full trip planning from the beginning. This is especially true when factoring in the inclusion of electric vehicles, and while widespread adoption may still be a few years away, personal preference should not be underrated.

About the 2023 Global Business Travel Forecast

Projections in the 2023 Global Business Travel Forecast involved:

-

Statistical models developed by GBTA -

Evaluation of historical price behavior and forecasts on air, hotel and ground categories by research, strategy and market and economic research firm, Avrio Institute -

The market-specific expertise and travel industry knowledge of CWT -

Information sourced from the International Monetary Fund Research Department, IATA, the World Travel and Tourism Council, the United Nations, and other leading organizations

Projections are based on anonymized transaction data from CWT's global client portfolio, including anonymized client travel patterns, over the past ten years. Key macroeconomic and per-country indicators, such as current and expected GDP growth, the consumer price index, unemployment rates and crude oil prices, were used in the statistical model, as well as key supply-side drivers sourced from OAG and STR Global. All air statistics represent point of origin and include all trip types.

▋ About GBTA

The Global Business Travel Association (GBTA) is the world's largest business travel and meetings trade organization representing the $1.4 trillion business travel industry. With operations across four continents, GBTA’s members manage more than $345 billion of global business travel and meetings expenditures annually. GBTA delivers world-class education, professional development, events, research, advocacy and media to a growing global network of more than 28,000 travel professionals and 125,000 active contacts.

▋ About CWT

CWT is a Business-to-Business-for-Employees (B2B4E) travel management platform. Companies and governments rely on us to keep their people connected – anywhere, anytime, anyhow – and across six continents, we provide their employees with innovative technology and an efficient, safe and secure travel experience. Every single day, we look after enough travelers to fill more than 100,000 hotel rooms, while our meetings and events division handles more than 100 events every 24 hours.

关注中航嘉信微信公众平台,

完美旅程由此开始!