【编者按】本文详述了AI资本开支周期的运作,并指出了目前美股极致分化的事实。泽元投资基金认为,在全球大市场的大气候下,中国市场小环境也呈现出类似的特征,值得投资者认真面对。

Feb. 24, 2026 10:40 PM ET

Summary

-

AI investment has contributed roughly $250 billion to US GDP, as capital expenditures by hyperscalers increased from $160 billion to an estimated $415 billion last year. -

Previous investment cycles have seen stocks peak 1-2 years before capital expenditures, and often while investments are still accelerating. -

As the AI arms race has accelerated, capital expenditures at several hyperscalers have surged to levels that now resemble regulated utilities. -

We are finding exceptional value among global defensives, which have fallen to their lowest weighting since 2000, leaving them trading at a discount. -

While the S&P itself rose by more than 17%, the World ex US posted its best year versus the S&P since 1993.

Parradee Kietsirikul/iStock via Getty Images

The railroads were a bubble and they transformed America. Electricity was a bubble, and it transformed America. The broadband build-out of the late-1990s was a bubble that transformed America. I am not rooting for a bubble ... but given the amount of debt now flowing into AI data center construction, I think it's unlikely that we're going to get out of this technology that isn't overbuilt and doesn't incur us a brief painful correction. - Derek Thompson, AI Could Be the Railroad of the 21st Century.——BY Broyhill

Source: Vanguard

Source: Vanguard

What the consensus appears to be overlooking, however, is that previous investment cycles have seen stocks peak 1-2 years before capital expenditures, and often while investments are still accelerating. The market doesn't wait for the last data center to be built. It doesn't care about the absolute level of investment. It sniffs out the change in growth. Notably, current estimates imply that growth rate is set to slow considerably this year.

Source: The Carlyle Group

Source: The Carlyle Group

Simply stated, investors have gotten plenty of experience spotting technological revolutions throughout history; but they haven't gotten much better at identifying the winners from those shifts. Turns out, there's little correlation between blistering growth and actual profitability, and a world of difference between the manufacturers of new technologies and the ultimate beneficiaries. The pattern is not coincidental. Firms flush with cash and intoxicated by optimism consistently overinvest in projects that generate poor returns on capital. The market rewards the spending — until it doesn't. Consider that the original bull case for today's hyperscalers rested on their capital-light business models, but while the stocks scale new highs, that thesis has quietly inverted.

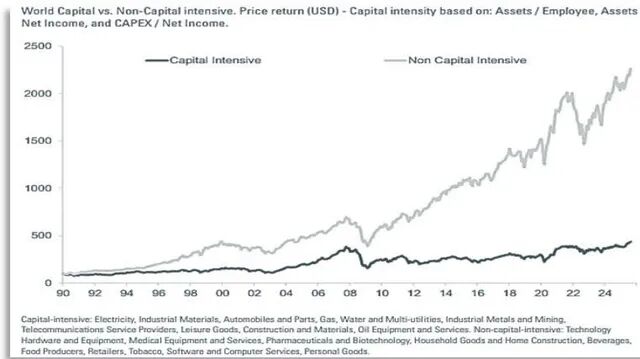

As the AI arms race has accelerated, capital expenditures at several hyperscalers have surged to levels that now resemble regulated utilities. The upside for utilities is that those investments are guaranteed a satisfactory rate of return. The downside of the AI arms race is that capital intensive companies tend to underperform over time.

World Capital vs. Non-Capital Intensive. Price return ('USD') - Capital intensity based on: Assets / Employee, Assets / Net Income, and CAPEX / Net Income.

Source: Goldman Sachs Global Investment Research

The silver lining? Initial investors and infrastructure builders suffered catastrophic losses. Still, those losses subsidized the creation of infrastructure for the users of that technology and the companies that built on top of it, who captured most of the economic value at a fraction of the cost.

This cycle appears to be playing out in a similar fashion, with businesses operating at the forefront of artificial intelligence changing hands at dizzying heights. But if AI proves to be as essential as electricity or the internet, the related economic gains will likely be just as diffuse, with benefits ultimately accruing to more traditional sectors of the economy that stand to gain meaningfully from productivity improvements, cost efficiency, and margin expansion. In a nutshell, value-oriented firms invest more cautiously and compound capital more efficiently. This would be consistent with history, as major economic transformations have often coincided with equity market transformations.

Where We See Value

The upside for investors is that there's no need to call the peak, duration, or ultimate winners of the AI cycle because there are plenty of other assets to choose from trading at compelling valuations. Said differently, tilting away from AI darlings does not require trimming equity exposure or accepting lower long-term expected returns, because investors are well compensated for taking on risk outside this narrow corner of the market today.

As a result, constructing a portfolio that doesn't rely on a continued AI-hype cycle without sacrificing upside is fairly easy. The hard part is having the courage and staying power to accept the enormous tracking error and the accompanying career risk that comes with deviating from concentrated, market-cap-weighted indices. Considering the magnitude of losses suffered by speculators throughout history's previous great technological shifts, increased tracking error seems like a small price to pay to avoid the potential for catastrophic financial losses.

Average percentile rank since 1925 in US equity market concentration, valuation, and magnitude of rally

Source: Goldman Sachs Global Investment Research

S&P 500 drawdown to subsequent three-year trough

Source: Goldman Sachs Global Investment Research

Encouragingly, market leadership has already begun to broaden, as the fourth quarter delivered a meaningful shift toward more diverse participation, and that shift has accelerated into the New Year. More encouragingly, we see ample runway for continued rotation, as dispersion remains elevated. In fact, in the three years since the launch of ChatGPT, cap-weighted indices have outperformed equal-weighted indices by more than 1,000 bps per year – a record more extreme than the tech bubble era and the most extreme on record. And contrary to popular opinion, earnings growth for both indices over the long term has been almost identical. Nearly all of the outperformance was driven by valuation.

Indexed NTM EPS

Source: Lyrical Asset Management, Factset

Now that investors are beginning to sniff out and appreciate the bargains on offer today, we think broad market leadership has a long way to go, as many assets outside US megacaps remain decidedly cheap. Against this backdrop, a number of opportunities stand out as particularly compelling. Value stocks everywhere are trading at some of the widest discounts on record. Nearly all sectors of the market outside of the world's largest companies have endured substantial multiple compression, with defensive equities at multi-decade lows, small- and mid-cap companies as cheap as they've been relative to large caps since the late 1990s, and opportunities abroad even more compelling. We believe this has created an extremely promising starting point for long-term outperformance.

US mid cap vs large cap stocks: relative 12m forward P/E

Source: Bank of America Global Investment Strategy

We are finding exceptional value among global defensives. These sectors have fallen to their lowest weighting since 2000, leaving them trading at a discount to both the market and their own histories, as sentiment has been deteriorating for years (chart below). Such dour sentiment is also evident in unusually high short interest, which creates the potential for meaningful buying pressure. From a portfolio construction standpoint, these sectors offer significant upside potential, and provide an element of defense, as big companies selling basic necessities tend to shine when the rest of the market is in trouble. Defensives have also historically been the best-performing sectors during rate-cutting cycles, with the added benefit of providing resilience if current AI enthusiasm proves misplaced or fades more quickly than expected.

Defensives Relative Forward P/e Ratio

Source: GQG Partners, Empirical Research Partners

S&P 500 defensive sector weight

Source: GQG Partners, Empirical Research Partners

Consider Nestlé (LVMUY) is a good example of the opportunities we see in Europe. LVMH is a French multinational conglomerate specializing in luxury goods, including fashion, leather goods, perfumes, cosmetics, watches, jewelry, and wines and spirits. It owns over 70 prestigious brands, combining heritage craftsmanship with global retail and marketing expertise. The company's earnings have been depressed due to a confluence of factors including luxury demand weakness across key markets, competitive shifts and market share dynamics, reduced profitability, and to some extent a lack of succession plan for Bernard Arnault. We think demand will return for luxury goods and with it will come improved profitability and a rerating in the stock.

Bottom Line

In a rare interview, Dan Sundheim, Founder of D1 Capital, was asked which company he'd own if he couldn't touch it for 10 years. His response, we think, was informative - not only because of what he said, but because of who said it.

There are very few tech companies I would say, I feel comfortable owning because tech just changes too quickly. So, it wouldn't be a tech company. It would have to be a company with a moat that would be incredibly difficult to penetrate with a growth rate that was probably not super high, but well above GDP for a long period of time.

Sundheim is not a casual observer of technology cycles. He built his career investing in technology across public and private markets, internet platforms, and emerging technologies, which is precisely why his answer matters. It's not a dismissal of AI. It's a warning that reflects an understanding that technological leadership is often fleeting, competitive advantages erode faster than expected, and long-term compounding depends less on narrative momentum than on durable economics.

That sentiment resonates deeply with our approach. Our priority has always been to compound capital prudently—not to chase every last dollar when risks are poorly understood, and returns depend on continued optimism rather than hard fundamentals. Our reluctance to participate in the AI frenzy has, without question, left money on the table. But like the circular financing of that party, we suspect that much of the capital being deployed with great enthusiasm today will ultimately find its way back to its rightful owners.

In our view, the market has increasingly come to resemble a concentrated, momentum-driven growth fund. This is not an environment in which we feel compelled to abandon discipline. If anything, it feels like a particularly poor moment to give up on cheap stocks with attractive assets, simply because they are unloved and being sold. So, we have no intention of replacing sound judgment with price momentum, chasing whatever philosophy happens to be working this quarter, or participating in the increasingly circular dynamics that characterize today's most crowded trades.

We have deliberately chosen not to follow that path. Very little of our portfolio is invested in stocks in broader market averages. Our portfolio looks nothing like the market. Relative to building data centers in space, it looks quite boring. And we find that comforting.

We are positioned exactly where we want to be. And exactly where we believe we should be. While we have rebalanced and refocused on higher conviction investments, with the majority of the portfolio invested in fresh names held for less than a year, our broader positioning remains consistent. We have maintained over 50% exposure to defensive sectors, over 50% allocated to small and mid-cap companies, and a significant allocation to businesses headquartered in Western Europe. We remain focused on identifying overlooked turnaround situations, significantly mispriced cyclical, and businesses undergoing multi-year transformations—often where capital is scarce, sentiment is poor, and patience is required. We are concentrated in undervalued, established businesses where returns are driven by actual cash flows and durable moats—not by dreams of future products dependent upon the ultimate success of trillions in speculative capital investments. We own businesses with recurring demand, defensible economics, and multiple self-help drivers to create value.

Notably, this positioning is not just Broyhill playing defense. It's the result of a decades-long process that leads us to opportunities where capital is scarce, where investors have abandoned opportunities, and where valuations and expected returns are as attractive as they've been in decades. In an overvalued equity market dependent upon never-ending capital expenditure and a chorus of circular deals and partnerships, we sleep well knowing that we own many outstanding businesses at a substantial margin of safety.

We did not execute perfectly last year. We have been candid about that. We revisited our positioning many times throughout the year to ensure we weren't confusing confidence with rigidity, and we course-corrected when the evidence demanded it. But to be clear, our mistakes were not due to a rejection of technology.

We aren't avoiding AI. We understand it. We appreciate it. We have invested in it and will continue to do so – at the right price. And we use it extensively. Internally, we have embraced AI aggressively to enhance our research process, improve monitoring, and accelerate decision-making. But from an investment perspective, we remain mindful that the greatest benefits of technological revolutions tend to accrue to users rather than producers—and that competitive forces eventually compress excess returns. So, rather than investing directly in technology, we have heavily invested in AI through companies we believe are set to gain the most from it.

History suggests that extreme divergences in valuation, as we see today, have often been followed by multi-year periods of excess returns to value. Over time, investing grounded in deep fundamental research has proven more profitable and more durable than chasing narratives or speculating on the promises of unproven technologies. We see no compelling reason to believe this cycle will be different. The weight of the evidence across economies and centuries remains clear: fundamentals and valuations matter.

We are keenly aware of the career risk that comes with sitting out the blow-off phase of a bull market. But we are equally aware of many more careers cut short by catastrophic losses. We've been doing this for over two decades and intend to keep doing it for at least two more. The trick to a lengthy career managing other people's money is threading the needle between analyzing fundamentals and accepting that markets routinely ignore them. Our willingness to accept discomfort while others follow the herd has historically been one of our greatest advantages—made possible by the long-term orientation of our partners.

For that trust, and that patience, we remain deeply grateful.

https://seekingalpha.com/article/4874266-the-ai-capital-cycle